Fill in Your 290 Arizona Form

The Arizona Form 290, known as the Request for Penalty Abatement, provides taxpayers an opportunity to request the Arizona Department of Revenue to abate (forgive) certain penalties due to reasonable cause and not willful neglect. This avenue is essential for individuals, businesses, corporations, trusts, and other entities facing penalties from non-audit assessments who can assert that circumstances beyond their control led to their inability to comply with tax obligations. To properly file a request, the taxpayer must provide comprehensive details including general information like taxpayer names, contact information, and specifics about the tax period and type. Furthermore, inclusion of Arizona Form 285, the General Disclosure/Representation Authorization Form, is necessary if the taxpayer wishes to have a representative communicate on their behalf. The form demands a clear articulation of the reasons for the abatement request, supported by relevant documentation such as canceled checks, medical reports, or death certificates, enhancing the request's credibility. It’s crucial to keep in mind that the form delineates specific signing requirements based on the entity type, ensuring the appropriate party authorizes the request. Initiatives to request penalty abatement using Form 290 are integral for those seeking relief from penalties imposed, allowing for a structured process to present their case to the Arizona Department of Revenue, with a processing time of up to six weeks.

Document Preview

Arizona Form 290 |

Request for Penalty Abatement |

UseTHE PURPOSEForm 290OFtoTHISrequestFORMan abatement of

The account for which the abatement request is being submitted must be in compliance. Compliance means there are no delinquent tax returns and all

The request will not be considered for processing if the form is incomplete or if the account is not in compliance. The abatement request form and documentation will be returned for correction. The form and documentation will then need to be resubmitted for consideration.

IMPORTANT: If the penalty being addressed is the result of an audit, do not use Form 290. Contact the Audit Unit at the phone number shown on the assessment. The Penalty Review Unit does not process audit assessed penalties.

INFORMATION

AllPARTrequests1 - GENERALfor abatementINFORMATIONof penalties must include the name, address, email address and telephone number of the taxpayer for which the request is being made.

If you want the Arizona Department of Revenue to work with your representative or third party, complete and include Arizona Form 285, General Disclosure/ Representation Authorization Form. Ensure boxes 4b and 4c or box 5 are indicated.

PART 2 - SPECIFIC DETAILS FOR ABATEMENT

ProvideCONSIDERATIONspecific details regarding the account and periods to be considered for abatement.

•TAXIfTYPEyour request is for an individual income tax return, use the Individual Taxpayer Identification Number (ITIN) number or social security number from the return.

• If your request is for a business account, use the Transaction Privilege Tax (TPT) or Marijuana Excise Tax (MET) license number.

• If your request is for a corporate or withholding account, use an Employer Identification Number (EIN).

EnterPERIOD(S)the specificOR YEAR(S)tax period(s) in date format, based on the filing frequency, that you want considered for the abatement.

For example:

• Annual filers:

• Quarterly filers:

• Monthly filers:

EnterPENALTYthe AMOUNTdollar amount for which you are requesting penalty abatement. There is no statutory provision that permits abatement of interest based on reasonable cause.

ExplainPART 3 - inEXPLANATIONdetail your&reason(s)DOCUMENTATIONfor requesting the abatement. You must provide specific details or reasons that directly contributed to the failure to file or pay timely for the period(s) you are requesting penalty abatement. Include in the explanation as to why there is reasonable cause for the returns and/or payments being late. Clear and concise information will allow for a prompt reply. Include additional pages if you need more space.

IMPORTANT: You must include Documentation that supports the basis of your request. Requests without

supporting documentation may be denied. Examples include:

• Proof of timely payment; including front and back of canceled checks.

• Medical reports and/or Death Certificate(s).

• Other pertinent documents that support your request for this abatement.

• Proof an extension has been filed.

BelowSituationsare someWh resituationsReasonablewhereCausereasonableMay Exist:cause may exist. There may be other situations where reasonable cause may exist. Accordingly, it’s important for you to provide specific details or reasons that directly contributed to the failure to. file or pay timely for the Circumstancesperiods you arebeyondrequestingthe control of the taxpayer while using reasonable and prudent business practices. A1.mathematicalMathematicalerroronrsa timely filed tax return.

2.Unexpected illness or unavoidable absence

A. aIndividual. Delay causedreturnsby serious illness of the taxpayer, or

member of the taxpayer’s immediate family. b. Delay caused by unavoidable absence of the

taxpayer. Vacation time is not acceptable as an unavoidable absence.

ADOR 11237 (05/23) |

Instructions |

Arizona Form 290 |

|

|

|

|

Request for Penalty Abatement |

||||||||||

|

|

B. Entity r turns |

|

|

|

|

|

|

If you want the Arizona Department of Revenue to work with |

||||||

|

|

|

In the caseof corporate, estate, trust or other business |

your representative or third party, complete and include |

|||||||||||

|

|

|

|

|

|

or |

|||||||||

|

|

|

returns, delay caused by unexpected serious illness of |

Arizona Form 285, General Disclosure/Representation |

|||||||||||

|

|

|

Authorization Form. Ensure boxes 4b and 4c box 5 are |

||||||||||||

|

|

|

the individual with sole authority to execute the return |

indicated. |

|

|

|

||||||||

|

|

|

or member of such individual’s immediate family. |

Handwritten signature, date, print the signer’s name and |

|||||||||||

|

|

|

Delay caused by unavoidable absence of the individual |

||||||||||||

If |

|

|

with sole authority to execute return. |

|

|

title. An electronic signature with a digital certificate is |

|||||||||

|

|

|

|

|

is the basis of the request for penalty |

accepted. |

|

|

|

||||||

abatement, the Department shall require proof of the date |

Type of Entity |

|

Who must sign |

|

|||||||||||

|

unexpected illness |

|

|

|

|

|

|

|

|

|

|

||||

of illness. This proof includes, but is not limited to, doctor |

|

|

|

|

|||||||||||

statements. |

|

|

|

|

|

|

|

Individuals, Joint |

The individual/joint filers/sole proprietor |

||||||

|

A. |

In the case of individual returns, delay caused by the |

Filers and Sole |

must sign. |

|

|

|||||||||

|

|

|

Proprietorships |

|

|

|

|||||||||

3. Death |

|

|

|

|

|

|

|

|

meaning of A.R.S. § |

||||||

death of a taxpayer or member of the taxpayer’s immediate |

|

||||||||||||||

family. |

|

|

|

|

|

|

|

Corporations |

A principal corporate officer within the |

||||||

|

|

|

|

|

|

|

|

person designated by a principal corporate |

|||||||

|

|

|

In the case of corporate, estate, trust or other business |

|

officer or any person designated in a resolution |

||||||||||

returns, the delay must have been caused by the death of an |

|

similar governing body, must sign. |

|||||||||||||

B. |

|

|

|

|

|

|

|

|

|

by the corporate board of directors or other |

|||||

individual with the sole authority to execute the return, or a |

|

|

|

|

|||||||||||

Limited Partnerships |

of the partnership must sign. |

|

|||||||||||||

member of such individual’s immediate family. |

|

|

|

||||||||||||

For both individual and business returns, a reasonable time |

Partnerships & |

A partner having authority to act in the name |

|||||||||||||

Trusts/Estates |

A trustee, executor/executrix or the personal |

||||||||||||||

frame should apply for filing the return and payment of tax. |

|

representative of the estate must sign. See |

|||||||||||||

A copy of the death certificate must be provided. |

|

|

|

Fiduciary Capacity. |

|

||||||||||

4. Absence of records |

|

|

|

|

|

Form 210, Notice of Assumption of Duties in a |

|||||||||

|

|

|

|

Limited Liability |

A member having authority to act in the name |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||

The taxpayer is unable to obtain records necessary to |

|||||||||||||||

Companies |

of the company must sign. |

|

|||||||||||||

determine the amount of tax due for reasons beyond the |

Governmental |

An officer having authority to act on behalf of |

|||||||||||||

taxpayer’s control. An example would be a fire which |

MAIL,AgenciesFAX OR EMAILtheFORMgovernmental290 TO:agency must sign. |

||||||||||||||

destroys the taxpayer’s records. |

|

|

|

|

|

|

|

||||||||

|

|

|

ARIZONA DEPARTMENT OF REVENUE |

||||||||||||

1. Ignorance of the law or lack of awareness of filing and |

|||||||||||||||

|

paying requirements. |

|

|

|

|

PENALTY REVIEW UNIT |

|

|

|||||||

Situations Where Reason ble C use May NOT Exist: |

|

1600 W MONROE ST |

|

|

|||||||||||

2. Delegation of duties. |

|

|

|

|

|

|

|||||||||

3. Financial difficulties have no effect on the taxpayer’s |

|

PHOENIX AZ |

|

||||||||||||

|

ability to file returns in a timely fashion. |

|

|

Fax No. (602) |

|

|

|||||||||

1. Interest |

|

|

|

|

|

|

|

Email: PenaltyReview@azdor.gov |

|

||||||

Penalti and/or fees not considered for Abatement: |

Allow up to six (6) weeks for processing. |

|

|||||||||||||

2. TPT licensing fees |

|

|

|

|

|

|

|

||||||||

3. Audit assessed penalties |

|

|

|

|

|

|

|

||||||||

4. Any disallowed accounting credit(s) for TPT |

|

|

|

|

|

|

|||||||||

For additional information regarding reasonable cause, |

|

|

|

|

|||||||||||

please refer to the following: |

|

|

|

|

|

|

|

||||||||

• Arizona Revised Statutes § |

|

|

|

|

|||||||||||

• |

|

|

www.azleg.gov. |

|

|

of Revenue |

|

Ruling |

|

|

|

|

|||

|

|

(GTR) |

|

|

|

General Tax |

|

and |

|

|

|

|

|||

|

|

|

Arizona Department |

of Revenue |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

Publication 700 |

|

|

|

|

|

|||

|

|

|

|

available at www.azdor.gov. |

|

|

|

|

|

|

|||||

PART 4 - SIGNATURE OF TAXPAYER OR AUTHORIZED TheREPRESENTATIVEform should be signed by one of those listed below or otherwise authorized by A.R.S. §

ADOR 11237 (05/23)

Print Form

Instructions

Arizona Form

290

Request for Penalty Abatement

PLEASE READ THE INSTRUCTIONS CAREFULLY. Ensure all applicable sections of the form are completed, all returns are filed, and taxes paid prior to submitting. The request will not be considered for processing if incomplete or the account is not in compliance. The abatement request form and

ThedocumentationArizona Departmentwill be returnedof Revenue,for correcon writtenion applicationnd must bebyresubmittedthe taxpayer,forshallconsiderationabate the penalty. if it determines that the conduct, or lack of conduct, that caused the penalty to be imposed was due to reasonable cause and not due to willful neglect.

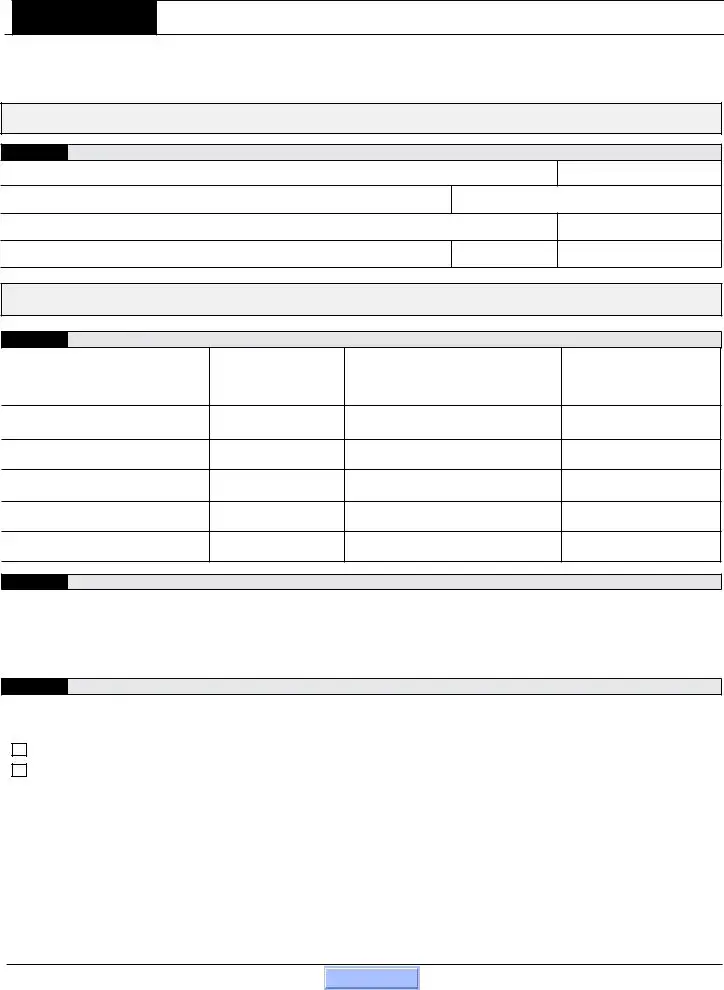

PART 1 |

GENERAL INFORMATION (REQUIRED) |

|

|

|

|

|

|||||

Taxpayer Name |

|

|

|

|

|

|

|

Daytime Phone (with area code) |

|||

Spouse’s Name (if joint return was filed) |

|

|

|

|

|

Email address: |

|

|

|

||

Present Address - number and street, rural route |

|

|

|

Apartment/Suite No. |

|

||||||

City, Town or Post Office |

|

|

|

|

|

|

State |

ZIP Code |

|

|

|

|

|

|

or |

|

|

|

|

|

|

|

|

If you want the Arizona Department of Revenue to work with your representative, complete and include Arizona Form 285, General Disclosure/Representation |

|||||||||||

Authorization Form. Ensure boxes 4b and 4c |

|

box 5 are marked. |

|

|

|

|

|

||||

PART 2 |

SPECIFIC DETAILS FOR ABATEMENT CONSIDERATION (REQUIRED) |

|

|

|

|||||||

|

TAX TYPE |

|

TAXPAYER ID |

|

Provide the |

SPECIFIC PERIOD(S) |

AMOUNT |

|

PENALTY |

||

Indicate the |

for the account |

|

Provide the associated |

|

Provide the total |

|

|||||

|

|

|

|

number for |

for the account requesting abatement |

|

for the account |

||||

requesting abatement |

|

the account requesting |

|

|

requesting abatement. |

||||||

Individual Income Tax |

|

|

ITIN or SSN |

|

|

(Do not include interest) |

|||||

|

abatement |

|

|

||||||||

|

|

|

|

|

|

|

|

|

$ |

|

|

License Number

$

EIN

$

EIN

$

EIN/License Number

$

PART 3 EXPLANATION & DOCUMENTATION (REQUIRED)

Provide specific details or reasons that directly contributed to the failure to file or pay timely for the periods you are requesting penalty abatement. Include additional pages if more space is needed and documentation to support the claim of reasonable cause.

_______________________________________________________________________________________________________________________________

PART 4 SIGNATURE OF TAXPAYER OR AUTHORIZED REPRESENTATIVE (Did you print and sign the form?)

Who can sign this form? The taxpayer (individual, principal corporate officer, LLC Member/Manager, Trustee, Partner) or other authorized by A.R.S. §

Check here if you are attaching a completed Arizona Form 285 with boxes 4b and 4c or box 5 indicated.

I certify that I have the authority, within the meaning of A.R.S. §

A.R.S. §

|

|

|

|

|

|

|

|

|

|

TAXPAYER’S SIGNATURE |

DATE |

SIGNATURE |

DATE |

|

|||

|

|

|

|

|

|

|

|

|

|

|

PRINT OR TYPE NAME |

|

|

|

PRINT OR TYPE NAME |

|

|

|

|

|

|

|

|

|

|

|

|

|

TITLE |

|

|

|

TITLE |

|

|

SEND THE COMPLETED FORM TO: ARIZONA DEPARTMENT OF REVENUE ● PENALTY REVIEW UNIT

●1600 W MONROE ST ● PHOENIX AZ

ADOR 11237 (05/23)

Print Form

File Properties

| Fact | Detail |

|---|---|

| Purpose of Form 290 | Used to request an abatement of non-audit penalties. |

| Exclusions | Not to be used for penalties resulting from an audit. |

| Essential Information Required | Must include name, address, and telephone number of the taxpayer. |

| Representation Authorization | If representation is desired, include Arizona Form 285. |

| Penalty Abatement Request Details | Specify tax type, Taxpayer ID Number, period or year, and penalty amount. |

| Explanation and Documentation | An explanation and supporting documentation for the penalty abatement request must be provided. |

| Authority to Sign Form 290 | Varies based on entity type (individual, corporation, partnership, etc.). |

| Governing Law | Arizona Revised Statutes § 42-1127 and § 42-2003 govern the procedure and authority related to penalty abatement. |

Instructions on Writing 290 Arizona

Once you've decided to request penalty abatement with the Arizona Department of Revenue, the Form 290 is your necessary next step. This document allows you to apply for the abatement of certain penalties provided that you can prove the penalty stemmed from reasonable cause rather than willful neglect. Filling out this form requires attention to detail and precision. Follow these steps to complete your request correctly and improve your chances of a successful outcome. Ensure you submit all required documentation to support your claim, as failure to do so may result in denial.

- Gather necessary documents and information, including the original penalty notice, any relevant financial statements, and other supporting documentation like medical reports or death certificates.

- Enter the Taxpayer Name, including the Spouse’s Name if a joint return was filed, along with your Daytime Phone and an Alternate Phone number.

- Provide your current Address, including apartment or suite number, City, Town or Post Office, State, and ZIP Code.

- If representation by another person is desired, remember to complete and attach Arizona Form 285, General Disclosure/Representation Authorization Form.

- In PART 2, specify the TAX TYPE that your request pertains to and provide the corresponding ID NUMBER (ITIN, SSN, License Number, or EIN) and the PERIOD(s) OR YEAR(s) related to the abatement request. Also, enter the PENALTY AMOUNT you’re requesting abatement for.

- In PART 3, explain in detail the reason(s) for your request. Include any circumstances that contributed to the situation that led to the penalty. Attach additional pages if more space is needed.

- Attach all pertinent documents that support your explanation. This can include, but isn't limited to, front and back copies of canceled checks, relevant tax returns, medical reports, death certificates, etc.

- Ensure the proper person signs and dates PART 4 of the form according to the type of entity filing the request (Individuals, Joint Filers and Sole Proprietorships, Corporations, Partnerships & Limited Partnerships, Trusts, Estates, Limited Liability Companies, or Governmental Agencies).

- Finally, mail or fax your completed Form 290, along with all supporting documents, to the PENALTY REVIEW UNIT, DIVISION 9 ARIZONA DEPARTMENT OF REVENUE 1600 W MONROE ST PHOENIX AZ 85007-2612. The fax number is 602-771-9912.

Expect the review process to take up to six weeks. For any questions or additional information, consult the Arizona Department of Revenue website or reach out directly to their office. Submitting Form 290 with thorough and accurate information, along with all necessary documentation, is crucial for the Arizona Department of Revenue to assess and potentially grant your request for penalty abatement.

Listed Questions and Answers

What is Arizona Form 290?

Arizona Form 290 is a document used to request the abatement of non-audit penalties from the Arizona Department of Revenue. A penalty abatement means that the department may forgive or cancel certain penalties if it's determined that the reason for the penalty was due to reasonable cause and not willful neglect.

Who can file Form 290?

Individual taxpayers, corporations, limited liability companies, trusts, estates, partnerships, and any other entity that has been assessed a penalty by the Arizona Department of Revenue for non-audit reasons can file Form 290.

What reasons qualify for a penalty abatement request?

Reasons may include circumstances beyond your control that prevented timely payment or filing, such as serious illness, natural disasters, or other significant events. The key requirement is to demonstrate that the penalty occurred despite reasonable care and effort to comply with tax laws.

What documents are needed to support a Form 290 request?

Supporting documentation is crucial for a successful abatement request. Examples include front and back copies of canceled checks, medical reports, death certificates, individual or business tax returns, and any other relevant documents that support the claim of reasonable cause.

Can a Form 290 request be made for penalties resulting from an audit?

No, Form 290 cannot be used for penalties resulting from an audit. If the penalty was assessed as a result of an audit, the taxpayer should contact the Audit Unit directly using the contact information provided in the assessment notice.

How long does it take to process a Form 290?

The Arizona Department of Revenue typically processes Form 290 requests within six weeks. This timeframe can vary depending on the complexity of the request and the completeness of the provided information.

Does filing a Form 290 guarantee that my penalties will be abated?

Filing a Form 290 does not guarantee that penalties will be abated. The Arizona Department of Revenue will review each request individually, considering whether the established criteria for reasonable cause have been met.

Who needs to sign Form 290?

The individual or entity making the request must sign Form 290. For joint filers, both spouses must sign. For corporations, a principal corporate officer or designated representative must sign. Similar signing requirements apply to partnerships, limited liability companies, trusts, estates, and governmental agencies, where the relevant authorized individual must sign.

Where should Form 290 be sent?

Completed Form 290 requests should be mailed or faxed to the Penalty Review Unit, Division 9, Arizona Department of Revenue, at the address or fax number provided on the form.

Can I authorize someone else to represent me in my Form 290 request?

Yes, if you want the Arizona Department of Revenue to work with your representative, such as a tax attorney or accountant, you should complete and include the Arizona Form 285, General Disclosure/Representation Authorization Form, together with your Form 290.

Common mistakes

Filling out the Arizona Form 290, the Request for Penalty Abatement form, can be a straightforward process, but mistakes can happen. These errors can delay the processing of your request or result in a denial. Avoiding common pitfalls can help ensure that your application is processed smoothly and efficiently. Here are seven mistakes people often make when completing this form:

- Not reading the instructions carefully before starting: It’s essential to understand the form’s requirements and gather all necessary information and documentation before filling out the form.

- Incomplete General Information section (Part 1): Every field in this section is crucial. Leaving out details like your full name, correct phone numbers, or address can cause issues in processing your request.

- Choosing the wrong Tax Type in Part 2: Selecting the incorrect tax type or providing the wrong Taxpayer ID Number can lead to your request being processed incorrectly or not at all.

- Forgetting to specify the tax period(s) or tax year(s): This information helps the Arizona Department of Revenue (ADOR) apply the abatement to the correct periods. Neglecting to enter this data can result in misapplied or rejected requests.

- Omitting penalty amount: Not specifying the amount for which you are requesting abatement can delay the evaluation process, as ADOR needs to know the scope of your request.

- Providing insufficient explanation in Part 3: The success of your request often hinges on the details within your explanation. Failing to clearly articulate the reasonable cause behind your request or neglecting to include supportive documentation can lead to a denial.

- Signature issues in Part 4: The form requires the proper signature to verify your authority and the authenticity of the request. An incorrect or missing signature can invalidate your entire application.

Moreover, people often forget that supportive documentation is vital to substantiate their claims for abatement. Whether it's bank statements, medical reports, or death certificates, including relevant documentation is crucial. Additionally, it is important to remember to use the correct form. If the penalty was a result of an audit, Form 290 is not applicable, and contacting the Audit Unit is necessary. The form clearly states this, yet it's a common oversight.

- Double-check each section for accuracy and completion.

- Ensure all supportive documentation is attached before submission.

- Use the form correctly and only for its intended purpose of requesting non-audit penalty abatements.

By steering clear of these common mistakes and following the detailed instructions provided by the Arizona Department of Revenue, individuals can navigate the Form 290 process more efficiently. A careful, well-documented request is more likely to result in a favorable outcome.

Documents used along the form

When dealing with Arizona Form 290, Request for Penalty Abatement, individuals often find themselves navigating through a maze of related documents and forms. This process not only involves understanding the direct implications and requirements of Form 290 but also engaging with additional documentation that supports or complements the abatement request. The completeness and accuracy of this information can significantly enhance the chances of a favorable outcome. Below is a list of documents commonly associated with Arizona Form 290, each serving a unique role in the penalty abatement process.

- Arizona Form 285, General Disclosure/Representation Authorization Form: This form permits the Arizona Department of Revenue to discuss and disclose tax information with a taxpayer's authorized representative.

- Power of Attorney (POA): A legal document granting an individual the authority to act on another's behalf in legal or financial matters, often used alongside Form 285 for representation in tax matters.

- Canceled Checks: Used as proof of payment, showing that an attempt was made to satisfy tax obligations within the stipulated period.

- Prior Year Tax Returns: These may help establish a pattern of compliance or explain discrepancies related to the penalty.

- Medical Reports: In cases where health issues are cited as the reason for penalty, these reports provide essential verification of the claims made.

- Death Certificates: Used to substantiate claims that a penalty was the result of circumstances related to a taxpayer’s or a family member’s death.

- Financial Statements: May be required to demonstrate financial hardship as the basis for abatement requests.

- Correspondence From the IRS: Letters or notices from the IRS relating to the tax issue under consideration can be crucial, especially if the federal tax status impacts the state tax situation.

- Court Documents: Legal documents relevant to cases of bankruptcy, divorce, or other court decisions that affect the taxpayer’s ability to pay the assessed penalties.

The interplay between Form 290 and these accompanying documents is critical. Successfully navigating the penalty abatement process requires a thorough understanding of both the primary requirements as set forth by the Arizona Department of Revenue and the ancillary documentation that supports those requests. Each document serves to build a comprehensive picture of the taxpayer’s situation, underlining the importance of meticulous record-keeping and proactive communication. In essence, the more substantiated information provided, the higher the likelihood of a favorable resolution.

Similar forms

The Arizona Form 290, used for requesting penalty abatement, bears similarities to the IRS Form 843, "Claim for Refund and Request for Abatement." Both forms are employed when a taxpayer seeks relief from penalties attributed to tax obligations, underscoring their focus on providing a statutory avenue to argue against penalties under certain circumstances. The primary distinction lies in their jurisdictional application, with Form 290 specific to Arizona state taxes and Form 843 applicable federally, through the IRS. This underscores a shared principle across different levels of tax authority, showing recognition of reasonable cause or other mitigating factors as valid grounds for penalty relief.

Similar to the Arizona Form 290, the IRS Form 656, "Offer in Compromise," provides taxpayers an opportunity to negotiate their tax liabilities, including penalties. While Form 290 specifically requests penalty abatement based on reasonable cause, Form 656 offers a broader negotiation for reducing overall tax debt under certain conditions, such as doubt as to liability and inability to pay. The convergence in their purpose highlights both forms' roles in alleviating financial burdens due to tax penalties, yet they diverge in scope with one targeting penalty relief and the other facilitating comprehensive tax debt resolution.

Another example is the Arizona Form 285, "General Disclosure/Representation Authorization Form." It is closely associated with Form 290 by facilitating the designation of a taxpayer’s representative in dealings with the Arizona Department of Revenue (ADOR). Although it doesn’t directly abate penalties, Form 285 is crucial for taxpayers who choose to have professionals navigate the penalty abatement process on their behalf, indicating an indirect but complementary relationship in managing and contesting tax penalties. This showcases how various forms work in tandem to support taxpayers in penalty and tax matters.

Similarly, the "Application for Extension of Time to File" forms, which exist both at the federal (IRS Form 4868) and state levels, share a preventative connection with Arizona Form 290. While not directly similar, they indirectly relate by providing taxpayers with a mechanism to avoid late-filing penalties through granted extensions. The existence of these forms underscores the tax system's flexibility and acknowledges that circumstances sometimes warrant additional time for taxpayers, thereby preventing situations that might later necessitate a Form 290.

The "Request for Waiver of Penalty" forms, used by many states including Arizona (Form 290), serve a similar administrative purpose across various jurisdictions. These forms, while varying in name and specific requirements, universally allow taxpayers to present arguments against the imposition of penalties due to reasonable cause. Such uniformity across states highlights a shared understanding within U.S. tax systems regarding the impact of penalties and recognizes the importance of providing a structured way for taxpayers to request relief.

Arizona's Taxpayer Advocate Service Request Form is yet another document aimed at assisting taxpayers encountering difficulties with the tax authorities, including issues related to penalties. Although it serves a broader purpose than the Form 290, its role in advocating for taxpayer rights and facilitating resolutions to tax-related problems connects it to the penalty abatement process. It represents another facet of the tax authority's commitment to fairness and responsiveness to taxpayer circumstances.

Form 433-A (OIC), the "Collection Information Statement for Wage Earners and Self-Employed Individuals," used by the IRS in evaluating offers in compromise, has a procedural linkage to Arizona Form 290. Even though Form 433-A deals with the collection process by assessing a taxpayer's financial situation for potential offer in compromise acceptance, it similarly reflects the system's flexibility in addressing taxpayers' inability to fully pay their tax liabilities, including penalties. This illustrates a broader theme of accommodating financial hardship in tax administration.

The IRS "First Time Abate (FTA)" administrative waiver is not a form per se but a policy that allows for abatement of certain penalties for the first time due to compliance history. This administrative relief shares the underlying philosophy with Arizona Form 290, emphasizing fairness and the recognition that compliant taxpayers can make mistakes. This comparison highlights how differing tools and policies within the tax systems aim to mitigate unintended punitive effects on otherwise compliant taxpayers.

State-specific "Innocent Spouse Relief" forms provide relief from tax liabilities, including penalties, for spouses unjustly held responsible for their partner's tax errors. While the Arizona Form 290 does not directly address innocent spouse situations, the broader principle of offering protections and reliefs to taxpayers under unfair circumstances is a common thread. Both avenues acknowledge the complexities of taxpayers' lives and offer recourse for relief, showcasing the tax system's adaptability to individual situations.

Finally, the "Installment Agreement Request" forms (e.g., IRS Form 9465) share a remedial purpose with Arizona Form 290. While Form 9465 focuses on allowing taxpayers to make scheduled payments on their tax liabilities to avoid or stop collection activities, it indirectly reduces the accumulation of additional penalties. This reflects an overall strategy within tax administration of preventing tax liabilities from becoming unmanageable and offering multiple pathways for taxpayers to remain in good standing.

Dos and Don'ts

Filling out the Arizona Form 290, the Request for Penalty Abatement, requires attention to detail and an understanding of what's expected. Below are key dos and don'ts that can guide you through the process, ensuring your request is clear, complete, and has the best chance of being favorably reviewed.

Things You Should Do:

Read the instructions carefully before you start. This ensures you know what information you need to gather and understand the form's requirements.

Include all required personal information such as your name, address, and phone number. If you're filing jointly, include your spouse's details as well.

Check the correct tax type related to your abatement request and use the appropriate taxpayer identification number.

Provide a detailed explanation for the abatement request. Explain the reasonable cause for the penalty, including any relevant events or circumstances, and attach all necessary documentation to support your claim.

Things You Shouldn't Do:

Don't forget to include Arizona Form 285 if you want the Arizona Department of Revenue to work with your representative. This form is essential for authorizing someone else to act on your behalf.

Avoid vague or incomplete explanations. Your request should clearly convey why you believe the penalty should be abated, supported by specific facts and documents.

Don't leave out any relevant tax periods or the penalty amount for which you're requesting abatement. This information is crucial for the Department of Revenue to assess your request properly.

Never submit the form without reviewing it for accuracy and completeness. Missing or incorrect information can delay the processing of your request or lead to a denial.

By following these guidelines, you can improve the clarity of your request and help the Arizona Department of Revenue understand your situation. Remember, the key is to provide a clear, complete, and well-supported argument for why the penalty should be abated.

Misconceptions

There are many misconceptions about Arizona Form 290, Request for Penalty Abatement, which can lead to confusion and errors when taxpayers attempt to use it. Here are eight common misunderstandings and the truths behind them:

- Misconception 1: Form 290 can be used for any type of penalty. In reality, Form 290 is specifically designed for the abatement of non-audit related penalties. Penalties resulting from an audit must be addressed directly with the Audit Division, not through Form 290.

- Misconception 2: A representative can be implicitly authorized to submit Form 290 on behalf of a taxpayer. However, to have a representative work with the Arizona Department of Revenue, the taxpayer must complete and include Form 285, clarifying the representative’s authority.

- Misconception 3: The form can be vague about the reason for penalty abatement. On the contrary, Form 290 requires a detailed explanation of the reasonable cause for the penalty, supported by clear and concise documentation.

- Misconception 4: Any document related to the penalty can serve as supporting documentation. Actually, only specific documents that directly support the reason for abatement, like medical reports or official records, are considered valid.

- Misconception 5: Form 290 applies to all tax types. The form is applicable only to certain tax types listed, such as Individual Income Tax and Corporate Income Tax, and the specific tax type must be clearly marked on the form.

- Misconception 6: Taxpayer ID numbers are optional. Taxpayer Identification Number (TIN) or Social Security Number (SSN) for individuals, and Employer Identification Number (EIN) or license number for businesses, must be provided for identification purposes.

- Misconception 7: The signature section is merely a formality. The signature certifies the authority of the signer and their knowledge of the penalties for submitting fraudulent or false documents. It is a critical part of the form that must be completed accurately.

- Misconception 8: The processing time for Form 290 requests is immediate. Processing can take up to six weeks, so patience is required after submission.

Understanding these misconceptions and addressing them correctly can significantly improve the chances of a successful penalty abatement request. It’s crucial for taxpayers to read the instructions carefully and ensure all necessary documentation is included to support their case clearly and concisely.

Key takeaways

Understanding the Arizona Form 290, designed for requesting penalty abatement, is crucial for taxpayers seeking relief from penalties due to reasonable causes. Here are key takeaways to ensure a successful application:

- Form 290 is specifically used to request the abatement of non-audit penalties. It's important to know that if the penalty you're dealing with is the result of an audit, you should instead contact the Audit Unit directly.

- When completing the form, accurate and complete general information is essential. This includes the taxpayer's name, daytime and alternate phone numbers, present address, and, if applicable, the spouse's name for joint returns.

- If a taxpayer wishes the Arizona Department of Revenue (ADOR) to work with a representative on their behalf, the Arizona Form 285, General Disclosure/Representation Authorization Form must be completed and included with the 290 form.

- The form requires you to specify the type of tax and provide related identification numbers, such as the ITIN, SSN, License Number, or EIN, depending on the tax type your request is associated with.

- Entering the specific tax period(s) or year(s) for which you are requesting penalty abatement is necessary to direct the request appropriately.

- An in-depth explanation and documentation supporting the reason for the late returns and/or payments must be provided. This explanation should clearly articulate the reasonable cause behind the delay.

- Documentation to support your claims is not just helpful; it's required. Examples of such documentation include copies of canceled checks, medical reports, death certificates, and any other pertinent documents that substantiate your request for abatement.

- The correct signature is imperative for the form to be processed. Depending on the entity type, such as individuals, corporations, partnerships, etc., the relevant party with the authority must sign the form.

- After submission, be prepared to wait up to six weeks for processing. This timeframe allows the ADOR to thoroughly review your request and make an informed decision.

It's also beneficial to familiarize yourself with the relevant Arizona Revised Statutes and the Arizona Department of Revenue's guidelines, which can provide further clarity on the abatement process. Properly filling out and submitting Form 290 can significantly impact the resolution of tax penalties for those who qualify for abatement.

Discover Common PDFs

How Much Does It Cost to File a Motion in Family Court - It explains the process for individuals needing to summon a witness or require the production of documents for a court case.

Azbon - Steps to achieve full approval for new nursing programs, emphasizing the importance of meeting Arizona Board of Nursing standards.

Arizona State Taxes Form - Through this form, employees can ensure that their state tax withholdings match their anticipated tax obligations.