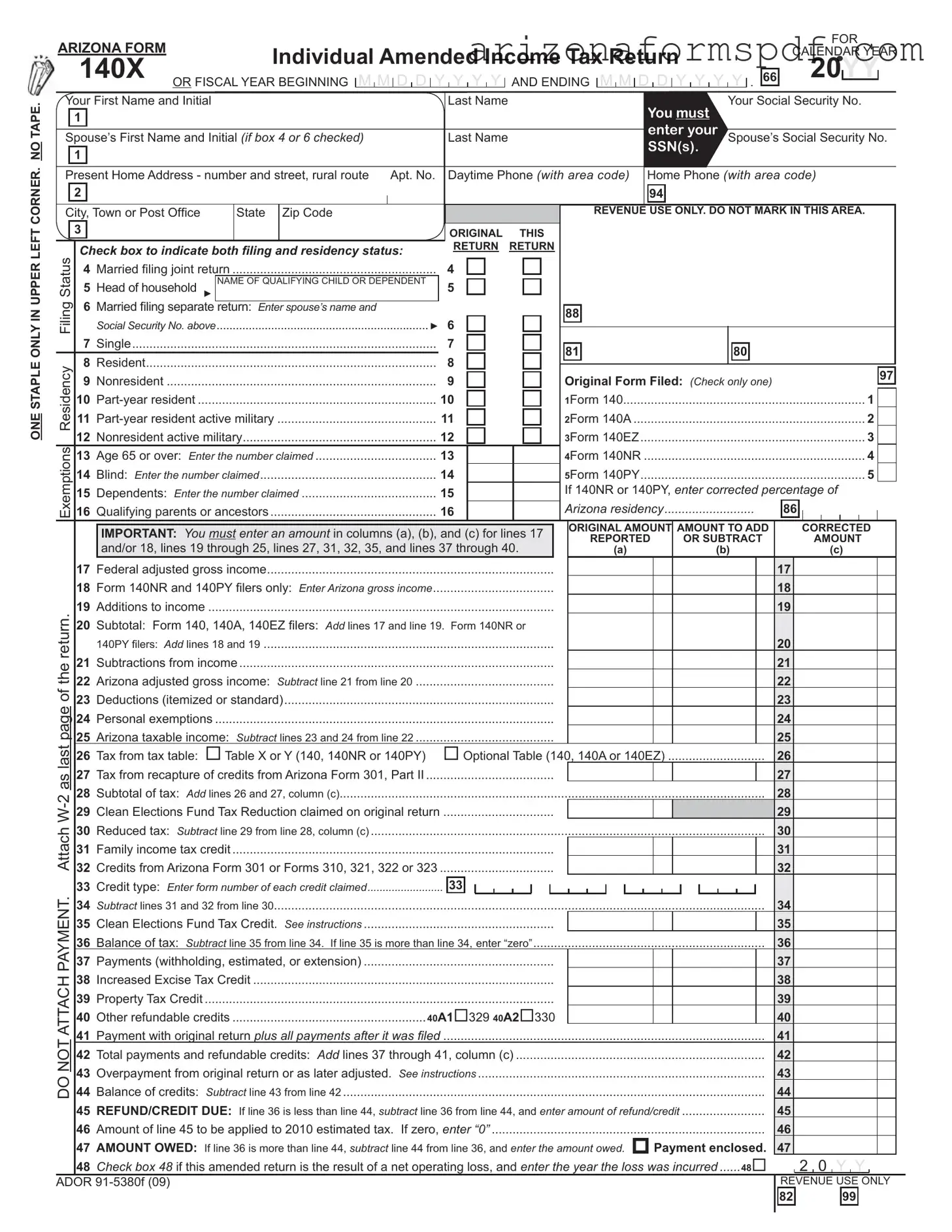

Fill in Your Arizona 140X Form

The Arizona 140X form is a crucial document for individuals seeking to amend their previously filed state income tax returns. This form caters to a variety of fiscal scenarios, whether adjustments are required for a calendar year or a fiscal period that does not align with the traditional calendar year. It is designed to accommodate changes in personal information, filing status, income, deductions, and credits that were not accurately reported on the original tax return. Essential components of the form include sections for recalculating tax obligations based on amended financial information, specifying reasons for amendments, and adjusting previously claimed dependents or exemptions. Moreover, the form provides space for detailing any payments made with the original return and calculating the net difference to determine if additional payment is due or if the taxpayer is eligible for a refund. This amendment process, facilitated by the Arizona 140X form, ensures taxpayers can correct discrepancies after the initial filing, maintaining compliance with Arizona tax laws. The form also underscores the importance of accuracy and transparency in tax reporting, offering a structured approach for taxpayers to rectify errors and update their financial records with the Arizona Department of Revenue.

Document Preview

ONE STAPLE ONLY IN UPPER LEFT CORNER. NO TAPE.

ARIZONA FORM |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

FOR |

|||||||||||||

|

|

Individual Amended Income Tax Return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CALENDAR YEAR |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

140X |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20 |

|

YY |

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

OR FISCAL YEAR BEGINNING |

|

M |

|

M |

|

D |

|

D |

|

Y |

Y |

Y |

|

Y |

|

AND ENDING |

|

M |

|

M |

|

D |

D |

|

Y |

|

Y |

|

Y |

Y |

|

. 66 |

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Your First Name and Initial |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Last Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Your Social Security No. |

|||||||||||||||||||||||||||||||||||

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

You must |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

enter your |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||

Spouse’s First Name and Initial (if box 4 or 6 checked) |

|

|

|

|

Last Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Spouse’s Social Security No. |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SSN(s). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Present Home Address - number and street, rural route Apt. No. |

Daytime Phone (with area code) |

|

Home Phone (with area code) |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

94 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City, Town or Post Office |

|

State |

Zip Code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

REVENUE USE ONLY. DO NOT MARK IN THIS AREA. |

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ORIGINAL |

THIS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

Check box to indicate both fi ling and residency status: |

|

|

|

|

RETURN RETURN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||

Status |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

4 |

|

Married fi ling joint return |

|

|

|

4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

5 |

Head of household. ► |

NAME OF QUALIFYING CHILD OR DEPENDENT |

|

|

|

|

5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Filing |

6 |

|

Married filing separate return: Enter spouse’s name and |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

88 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

.................................................................. |

|

|

|

|

|

|

|

|

|

|

|

► 6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

Social Security No. above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

7 |

|

Single |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

|

|

|

|

|

|

|

|

|

|

|

81 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

80 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Residency |

8 |

|

Resident |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

97 |

|

|||||||||||||||||||||||||||

9 |

|

Nonresident |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

9 |

|

|

|

|

|

|

|

|

|

|

|

|

Original Form Filed: (Check only one) |

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||

10 |

|

|

|

|

|

|

|

|

|

|

|

|

10 |

|

|

|

|

|

|

|

|

|

|

|

|

1Form 140 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

|

|

||||||||||||||||||||||||||||||||

11 |

|

11 |

|

|

|

|

|

|

|

|

|

|

|

|

2Form 140A |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2 |

|

|

|

|||||||||||||||||||||||||||||||||||||||||||

12 |

|

Nonresident active military |

12 |

|

|

|

|

|

|

|

|

|

|

|

|

3Form 140EZ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

|

|

||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||

Exemptions |

13 |

|

Age 65 or over: Enter the number claimed |

13 |

|

|

|

|

|

|

|

|

|

|

|

|

4Form 140NR |

................................................................ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

|

|

|||||||||||||||||||||||||||||||||||||||||

14 |

|

Blind: Enter the number claimed |

14 |

|

|

|

|

|

|

|

|

|

|

|

|

5Form 140PY |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

|

|

||||||||||||||||||||||||||||||||||||||||||

15 |

|

Dependents: Enter the number claimed |

15 |

|

|

|

|

|

|

|

|

|

|

|

|

If 140NR or 140PY, enter corrected percentage of |

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||

16 |

|

Qualifying parents or ancestors |

16 |

|

|

|

|

|

|

|

|

|

|

|

|

..........................Arizona residency |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

86 |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

IMPORTANT: You must enter an amount in columns (a), (b), and (c) for lines 17 |

|

|

ORIGINAL AMOUNT |

AMOUNT TO ADD |

|

|

CORRECTED |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

REPORTED |

OR SUBTRACT |

|

|

|

|

AMOUNT |

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

and/or 18, lines 19 through 25, lines 27, 31, 32, 35, and lines 37 through 40. |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

|

|

|

|

|

|

|

|

|

|

|

|

(b) |

|

|

|

|

|

|

(c) |

|

||||||||||||||||||||||||||||||||||||||||||||||||

|

|

17 |

|

Federal adjusted gross income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

17 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

18 |

|

Form 140NR and 140PY fi lers only: Enter Arizona gross income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

return. |

19 |

|

Additions to income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

20 |

|

Subtotal: Form 140, 140A, 140EZ filers: Add lines 17 and line 19. |

Form 140NR or |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||

|

|

|

140PY filers: Add lines 18 and 19 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

21 |

|

Subtractions from income |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

21 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

the |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

22 |

|

Arizona adjusted gross income: Subtract line 21 from line 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

23 |

|

Deductions (itemized or standard) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

23 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

page |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

24 |

|

Personal exemptions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

25 |

|

Arizona taxable income: Subtract lines 23 and 24 from line 22 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

25 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

last |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

26 |

|

Tax from tax table: |

Table X or Y (140, 140NR or 140PY) |

|

|

|

|

Optional Table (140, 140A or 140EZ) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||

|

27 |

|

Tax from recapture of credits from Arizona Form 301, Part II |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

27 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

as |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

28 |

|

Subtotal of tax: Add lines 26 and 27, column (c) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

28 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

W- |

29 |

|

Clean Elections Fund Tax Reduction claimed on original return |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

29 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Attach |

30 |

|

Reduced tax: Subtract line 29 from line 28, column (c) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

31 |

|

Family income tax credit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

31 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

32 |

|

Credits from Arizona Form 301 or Forms 310, 321, 322 or 323 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

32 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

PAYMENT. |

33 |

|

Credit type: Enter form number of each credit claimed |

|

|

|

|

33 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

34 |

|

..............................................................................................................................................Subtract lines 31 and 32 from line 30 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

34 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

35 |

|

Clean Elections Fund Tax Credit. See instructions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

36 |

|

Balance of tax: Subtract line 35 from line 34. If line 35 is more than line 34, enter “zero” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

36 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

37 |

|

Payments (withholding, estimated, or extension) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

37 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

ATTACH |

38 |

|

Increased Excise Tax Credit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

38 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||

39 |

|

Property Tax Credit |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

39 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

40 |

|

Other refundable credits |

40A1 329 40A2 |

330 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

40 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||

41 |

|

Payment with original return plus all payments after it was filed |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

41 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||

NOT |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

42 |

|

Total payments and refundable credits: Add lines 37 through 41, column (c) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

42 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||

|

43 |

|

Overpayment from original return or as later adjusted. See instructions |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

43 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

DO |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||||||

44 |

|

Balance of credits: Subtract line 43 from line 42 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

44 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

|

|

45 |

|

REFUND/CREDIT DUE: If line 36 is less than line 44, subtract line 36 from line 44, and enter amount of refund/credit |

........................ |

|

|

|

|

|

|

|

|

|

|

|

|

45 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

46 |

|

Amount of line 45 to be applied to 2010 estimated tax. If zero, enter “0” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

46 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||||||

|

|

47 |

|

AMOUNT OWED: If line 36 is more than line 44, subtract line 44 from line 36, and enter the amount owed. |

|

|

Payment enclosed. |

47 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

|

|

48 |

|

Check box 48 if this amended return is the result of a net operating loss, and enter the year the loss was incurred |

48 |

|

|

|

2 0 Y Y |

|||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

ADOR |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

REVENUE USE ONLY |

|||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

82 |

|

99 |

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

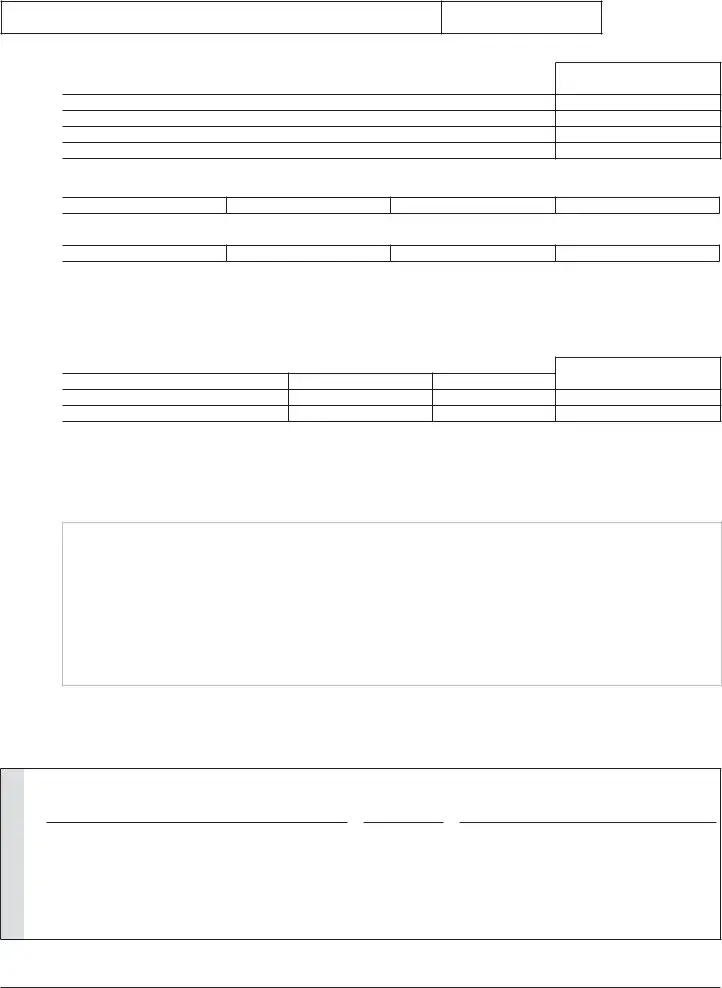

Your Name (as shown on page 1)

Your Social Security No.

PART I: Dependent Exemptions - do not list yourself or spouse as dependents

List children and other dependents. If more space is needed, attach a separate sheet.

FIRST AND LAST NAME: |

SOCIAL SECURITY NO. |

RELATIONSHIP |

|

|

|

NO. OF MONTHS LIVED IN YOUR HOME DURING THE TAXABLE YEAR

Enter the names of the dependents listed above who do not qualify as your dependent on your federal return:

Enter dependents listed above who were not claimed on your federal return due to education credits:

PART II: Qualifying Parents and Ancestors of Your Parents Exemptions (Arizona residents only)

List below qualifying parents and ancestors of your parents for which you are claiming an exemption. If more space is needed, attach a separate sheet. Do not list the same person here that you listed in Part I, above, as a dependent. For information on who is a qualifying parent or ancestor of your parents, see the instructions for the original return that you filed.

FIRST AND LAST NAME:

SOCIAL SECURITY NO.

RELATIONSHIP

NO. OF MONTHS LIVED IN YOUR HOME DURING THE TAXABLE YEAR

PART III: Income, Deductions, and Credits

List the line reference from page 1 for which you are reporting a change then give the reason for each change. Attach any supporting documents required. If the change(s) pertain(s) to an IRS audit, please attach a copy of the agent’s report. If you filed an amended federal return with the IRS (Form 1040X), please attach a copy and all supporting schedules.

Part IV: Name and Address on Original Return

If your name and address is the same on this amended return as it was on your original return, write “same” on the line below.

Name |

Number and Street, R.R. |

Apt. No. |

City, Town or Post Office State Zip Code |

|

|

|

|

PLEASE SIGN HERE

I have read this return and any attachments with it. Under penalties of perjury, I declare that to the best of my knowledge and belief, they are true, correct and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

YOUR SIGNATURE |

|

|

|

|

DATE |

|

|

OCCUPATION |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

SPOUSE’S SIGNATURE |

|

|

|

|

DATE |

|

|

SPOUSE’S OCCUPATION |

||||

|

|

|

|

|

|

|

|

|

|

|

||

PAID PREPARER’S SIGNATURE |

|

|

DATE |

|

|

|

FIRM’S NAME (PREPARER’S IF |

|||||

|

|

|

|

|

|

|

|

|

|

|

||

PAID PREPARER’S TIN |

PAID PREPARER’S ADDRESS |

|

|

|

|

|

|

|

PAID PREPARER’S PHONE NO. |

|||

If you are sending a payment with this return, mail to Arizona Department of Revenue, PO Box 52016, Phoenix, AZ,

If you are expecting a refund or owe no tax, or owe tax but are not sending a payment, mail to Arizona Department of Revenue, PO Box 52138, Phoenix, AZ,

ADOR |

Form 140X (2009) |

Page 2 of 2 |

File Properties

| Fact | Description |

|---|---|

| Form Title | Arizona Form 140X |

| Purpose | For filing an Individual Amended Income Tax Return |

| Usage | Used by taxpayers who need to amend their previously filed income tax return | >

| Applicable Years | Can be used for any calendar year (20YY) or fiscal year beginning and ending dates |

| Filing Options | Includes options for varying filing statuses and residency (resident, nonresident, part-year resident) |

| Governing Laws | Arizona Revised Statutes and regulations pertaining to state income tax |

| Submission Addresses | Separate mailing addresses provided depending on payment or refund status |

| Special Instructions | Instructions specify "ONE STAPLE ONLY IN UPPER LEFT CORNER. NO TAPE." indicating submission preferences |

Instructions on Writing Arizona 140X

Filling out the Arizona Form 140X, an amended individual income tax return, is an important process for residents who need to correct or update their income tax filings. Whether changes stem from an audit, a discovered error, or an omission on the original return, completing this form ensures that your tax obligations are accurate and up to date. Carefully following these steps will guide you through the process, helping to ensure that the information you provide is correct and that the form is submitted properly.

- Place one staple in the upper left corner of the form if you have additional documents to attach.

- Write the calendar year or fiscal year that is being amended at the top of the form, specifying the beginning and ending dates using the format MMDDYYYY.

- Enter your first name, initial, and last name, along with your Social Security Number in the designated spaces.

- If you are amending a joint return, you must also enter your spouse's first name, initial, last name, and Social Security Number.

- Provide your present home address, including the apartment number if applicable, and both your daytime and home phone numbers with area codes.

- Indicate your filing and residency status by checking the appropriate boxes for your situation (e.g., Married filing joint return, Head of household, Single, Resident, Nonresident).

- Specify the original form you filed by checking the corresponding box.

- Enter information about exemptions, such as age, blindness, and number of dependents.

- Fill in the financial sections, including federal adjusted gross income, additions and subtractions from income, deductions, personal exemptions, and the corrected amount of Arizona adjusted gross income, and then calculate the taxable income.

- Determine and enter the tax from the tax table or optional tax tables, any recapture of credits, and calculate the subtotal of tax.

- Adjust for any claimed Clean Elections Fund Tax Reduction from the original return.

- List any credits from Arizona Form 301 or Forms 310, 321, 322, or 323, and calculate the adjusted balance of tax owing or refundable.

- Document payments and refundable credits, including withholding, estimated payments, payments made with the original return, and any other refundable credits.

- Calculate the overpayment from the original return and the balance of credits, then enter the amount of refund or credit due, or amount owed.

- If applicable, check the box if this amended return is the result of a net operating loss.

- Provide the name and address as it appeared on the original return, or write "same" if there are no changes.

- Read the declaration at the end of the form, then sign and date it. If filing jointly, your spouse must also sign and date the form.

- If you used a paid preparer, ensure the preparer signs the form and provides their information as directed.

- Mail the completed form to the appropriate Arizona Department of Revenue address, depending on whether you are submitting a payment or requesting a refund or if there is no change in the amount owed.

After submitting the Arizona 140X form, the Department of Revenue will process your amended return. This process can take some time, so it’s important to wait patiently. You might receive a notice or request for additional information, so keep all relevant documents handy. Correcting your tax return is a responsible step toward ensuring your tax information is accurate and up to date.

Listed Questions and Answers

What is the purpose of the Arizona Form 140X?

The Arizona Form 140X is an Individual Amended Income Tax Return form designed for residents who need to correct or update their previously filed state income tax return. This could be necessary due to mistakes, omissions, or changes in tax status that occurred after the original submission. The form allows taxpayers to amend their income, deductions, credits, and payments to ensure accurate tax liability and compliance with state tax laws.

When should I file the Arizona Form 140X?

Form 140X should be filed after you realize there was an error or change needed to a previously filed Arizona state income tax return. It's crucial to file this amended return as soon as possible to correct any inaccuracies. However, there are deadlines for certain changes, especially if you're expecting a refund. Generally, you must file Form 140X within four years from the date you filed your original tax return or within one year after the date the original tax was paid, whichever is later.

Can I file Form 140X electronically?

As of the latest available information, the Arizona Department of Revenue encourages electronic filing for many forms, but it's essential to check the current filing options for Form 140X specifically. The department’s website or a tax professional can provide the most current filing methods and any updates on electronic submission availability for amending your return.

What documentation do I need to attach with Form 140X?

When filing a Form 140X, you should attach any supporting documents related to the changes being made to your tax return. This includes any corrected W-2s, 1099s, schedules, and if applicable, a copy of your amended federal income tax return (Form 1040X) along with all supporting documentation. If your changes are due to an IRS audit, attach a copy of the IRS audit report. Always ensure you provide comprehensive documentation to support your amendments.

How do I determine if I owe money or am due a refund after amending my tax return?

After completing Form 140X, you will calculate the corrected tax liability and compare it to what was previously paid. If the amended return shows that you owe additional tax, you should pay this amount to avoid potential penalties and interest. Conversely, if you find that you have overpaid based on the corrected information, you can request a refund. The form includes sections to calculate the corrected tax, any additional payments owed, or the refund amount that may be due. Ensure to review these calculations carefully to understand your tax position following the amendment.

Common mistakes

Filling out tax forms can be a complex process, with the Arizona 140X form being no exception. People often make mistakes while attempting to amend their income tax returns. Identifying and understanding these common errors can help ensure that corrections are submitted accurately, preventing unnecessary delays or issues with the Arizona Department of Revenue. Here are ten mistakes to avoid:

- Not using a single staple in the upper left corner. The instructions clearly state that only one staple should be used, and it should be placed in the upper left corner. Using more than one staple or placing it in a different location can cause processing delays.

- Applying tape to the form. The form specifies "NO TAPE," yet people often use tape on their documents, which can cause problems with the processing equipment.

- Incorrectly entering names and social security numbers. For oneself or a spouse, especially if box 4 or 6 is checked, it's crucial to enter this information accurately to match IRS records.

- Filling out the residency section inaccurately. The form requires marking the correct residency status, yet this is often overlooked or filled out incorrectly.

- Not indicating the correct original form filed. The amended return asks for the original form filed (1Form 140, 2Form 140A, etc.), which is frequently left blank or incorrectly marked.

- Omitting required amounts in columns (a), (b), and (c). For specific lines, all three columns must be completed, but filers often miss adding amounts to one or more columns.

- Incorrectly reporting federal adjusted gross income and Arizona gross income. These figures are critical for accurate processing but are prone to errors by filers.

- Not accurately detailing exemptions such as age 65 or over, blind, dependents, and qualifying parents or ancestors. These exemptions have specific criteria and are often either mistakenly claimed or overlooked.

- Forgetting to attach necessary supporting documents when reporting changes. Any change reported on the form must be accompanied by relevant documents, yet filers frequently forget to include them.

- Failing to sign and date the form or including the preparer's information if applicable. This common oversight renders the form incomplete and unable to be processed.

By paying close attention to these frequent errors and reviewing the form carefully before submission, filers can improve the accuracy of their amended returns and facilitate smoother processing by the Arizona Department of Revenue.

Documents used along the form

Filing an amended tax return, particularly the Arizona Form 140X for Individual Amended Income Tax Return, is a process that often involves including additional forms and documents to support the changes being reported. The purpose of amending a return can vary, ranging from correcting errors to reporting additional income or claiming missed deductions and credits. To accurately address these adjustments, taxpayers may need to submit several other documents alongside Form 140X. Understanding these documents ensures that the amendment process is handled efficiently, minimizing delays or issues with processing.

- Form 1040X: This is the Federal Amended U.S. Individual Income Tax Return. If changes to your federal income tax return affect your state tax liability, it's crucial to include a copy of this form. It provides an overview of the adjustments made to your federal tax return, which may have implications for your state tax due.

- W-2 Forms: These are Wage and Tax Statements from your employer. You may need to submit corrected or additional W-2 forms if your income was reported incorrectly or omitted from your original state tax return.

- Form 1099: This includes various types of income outside of wages, such as interest, dividends, government payments, and more. Submitting additional or corrected 1099 forms is essential if this income was not accurately reported initially.

- Schedule A (Form 1040): If you're claiming itemized deductions on your Arizona return that differ from what was originally filed, including a copy of Schedule A can provide the necessary details. This is particularly relevant if your deductions on the federal level have changed.

- Schedule C (Form 1040): For those who are self-employed, this form details the profit or loss from a business. A revised Schedule C might be necessary if your business income or expenses were not correctly reported on your original tax return.

- Documentation of Payments: This includes records of any estimated tax payments made, withholding documented on W-2s or 1099s, and any other payments towards your tax liabilities. These documents help reconcile any differences in payments owed or refunds due based on the amendments made.

Submitting these documents in conjunction with your Arizona Form 140X is vital for a thorough review and processing of your amended tax return. Each piece of documentation supports your claim and provides clarity on the adjustments you're reporting. Remember, the goal is to ensure that your tax obligations are met accurately, reflecting all income, deductions, and credits you're entitled to. Assisting in this process by preparing these documents can expedite processing and ensure your amended return is accepted and processed without delay.

Similar forms

The Arizona Form 140X, an Individual Amended Income Tax Return, shares similarities with the Internal Revenue Service (IRS) Form 1040X, which is the Amended U.S. Individual Income Tax Return. Both forms serve the purpose of making corrections to previously filed income tax returns. They allow taxpayers to adjust income, deductions, credits, and calculate the difference in tax owed or refund due. Furthermore, each requires the taxpayer to provide a detailed explanation for the amendments, ensuring transparency and accuracy in the tax reporting process.

Another document akin to Arizona Form 140X is Form 1040, the U.S. Individual Income Tax Return. This form is the starting point for individual tax filing, placing a foundation for the 140X. Whenever changes occur that necessitate an amendment, the 140X form acts as the 1040's counterpart at the state level for Arizona residents. Both involve reporting personal income, tax deductions, credits, and calculating tax liability, although the 140X is specifically designed for corrections post-original submission.

Form 140NR, Nonresident Personal Income Tax Return, also bears resemblance to the 140X, mainly when nonresidents need to amend their tax returns. Adjustments to a nonresident's income earned in Arizona, deductions, or credits can lead to the filing of a 140X form, specifically when correcting a 140NR submission. The process underscores the importance of accurate tax reporting for nonresidents and the mechanism for rectifying any misreporting.

Similar to the 140X is the Form 140PY, the Part-Year Resident Personal Income Tax Return for Arizona. This form caters to individuals who have resided in Arizona for only a portion of the tax year. Should there be errors or necessary updates to the original part-year resident return, the 140X form steps in to facilitate these amendments, mirroring the correction process of the 140PY by allowing adjustments to income, deductions, and credits based on Arizona residency duration.

The Arizona Form 301, Nonrefundable Individual Tax Credits and Recapture, also interacts closely with the 140X, particularly in the adjustment of tax credits. If a taxpayer needs to amend credits originally claimed on Form 301, the 140X provides the avenue to report these changes. This highlights the fluidity and interconnectedness between claiming tax credits and the necessity to amend those claims when inaccuracies are discovered post-filing.

Significantly akin to the 140X is Arizona Form 322, Credit for Contributions to Charities That Provide Assistance to the Working Poor. When taxpayers contribute to qualifying organizations and claim this credit, errors or changes in the claimed amount may later necessitate amendments through the 140X form. This scenario underscores the potential need for adjustments in tax benefits derived from charitable contributions, illustrating another layer of tax management and correction enabled by the 140X.

Lastly, the relationship between Form 140X and Arizona Form 202, Credit for Taxes Paid to Another State or Country, is noteworthy. For Arizona taxpayers who must amend the credit claimed for taxes paid to another jurisdiction, the 140X serves as the corrective vehicle. This context reveals the complexity of managing tax obligations across different tax jurisdictions and the role of the 140X in ensuring accurate tax reporting and relief for taxes paid elsewhere.

Dos and Don'ts

When filling out the Arizona 140X form, it is important to consider both the steps you should follow and the mistakes you should avoid to ensure the process is completed properly and efficiently. Here are fundamental guidelines:

Things You Should Do:

Review the original return: Before making amendments, thoroughly review your original tax return. This ensures you understand what changes need to be made and can accurately report them on the 140X form.

Attach all required documents: If your amendments are due to changes in your income, deductions, credits, or dependents, ensure all necessary documentation supports these changes. This includes any relevant forms or schedules that substantiate your amendment.

Sign and date the form: Ensure that you (and your spouse, if filing jointly) sign and date the 140X form. An unsigned form is considered invalid and can lead to processing delays.

Use the correct mailing address: Depending on whether you are expecting a refund, owe no tax, or are making a payment, the mailing address will differ. Double-check the appropriate address to avoid any delays in processing.

Things You Shouldn't Do:

Staple or tape documents excessively: The form specifies to use one staple only in the upper left corner if needed. Avoid using tape or multiple staples as this can hinder the processing of your form.

Ignore the residency section: If there have been any changes to your residency status, or if you're correcting previously reported information, make sure this section is completed accurately to avoid issues with your tax calculation.

Forget to amend state return after amending federal return: If you’ve amended your federal return, it’s crucial to also amend your state return if those federal changes affect your state tax liability.

Fail to include the payment if you owe: If the amendment results in you owing additional tax, make sure to include the payment when you mail your 140X form. Neglecting to do so could result in interest and penalties.

Misconceptions

When dealing with the complexities of tax returns, especially amended ones, it's easy to encounter misunderstandings. The Arizona Form 140X, utilized for amending individual income tax returns, is no exception. Let's clear up some common misconceptions:

It's only for errors: While commonly used to correct mistakes, Form 140X is also for making adjustments such as claiming an overlooked deduction or credit.

Amendments delay refunds for years: Although amending a return can take longer to process, most are completed within a few months, not years.

Electronically filing is an option: As of the last update, the Arizona Department of Revenue does not accept Form 140X electronically; it must be mailed.

Amendments always lead to audits: Filing a 140X does not automatically trigger an audit. Amendments are a standard part of tax administration.

No deadline for filing: There is a general misconception that amendments can be filed at any time. However, generally, you have up to four years from the due date of the return to file Form 140X.

Original return doesn’t matter: When filing a 140X, it is crucial to reference the original tax return filed. Failing to do so may result in processing errors or delays.