Fill in Your Arizona 285 Form

The Arizona 285B Disclosure Authorization Form serves a pivotal role in the dynamics of tax information sharing by allowing specified appointees to access confidential taxpayer information, without conferring them any powers of representation. Upon completion, which mandates signing in section 5 to validate, this document empowers the Arizona Department of Revenue to release details about the taxpayer(s) to designated appointee(s) for specific tax types detailed within the form. Taxpayer information required includes names, Social Security Numbers (SSNs) or Individual Tax Identification Numbers (ITINs), and contact details; appointees must share similar information alongside their identification numbers. Moreover, the form enumerates tax types and the pertinent tax years or periods, clarifying the scope of information shared. Importantly, it clarifies that signing this form does not revoke any pre-existing authorization(s) or Power of Attorney documents on file. The legal implications are underscored by a certification process where signatories affirm their authority to execute this authorization on behalf of the taxpayer(s), alerting them to the seriousness of presenting fraudulent or false documents, classified under Arizona law as a class 5 felony.

Document Preview

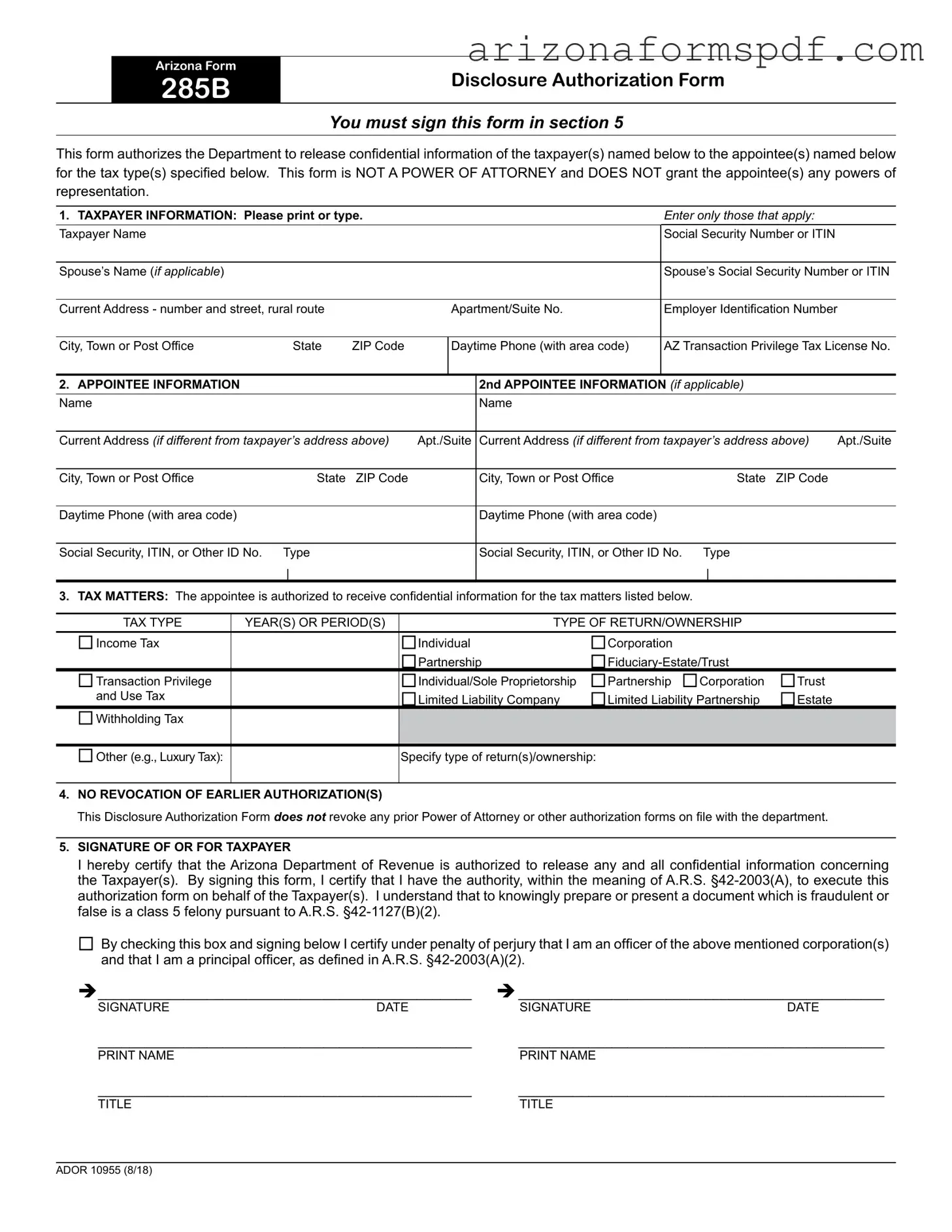

ARIZONA FORM

285B

DISCLOSURE AUTHORIZATION FORM

You must sign this form in section 5

This form authorizes the Department to release confidential information of the taxpayer(s) named below to the appointee(s) named below for the tax type(s) specified below. This form is NOT A POWER OF ATTORNEY and DOES NOT grant the appointee(s) any powers of representation.

1. TAXPAYER INFORMATION: Please print or type. |

|

|

|

Enter only those that apply: |

|

||

Taxpayer Name |

|

|

|

|

|

Social Security Number or ITIN |

|

|

|

|

|

|

|

|

|

Spouse’s Name (if applicable) |

|

|

|

|

|

Spouse’s Social Security Number or ITIN |

|

|

|

|

|

|

|

|

|

Current Address - number and street, rural route |

|

|

Apartment/Suite No. |

Employer Identification Number |

|

||

|

|

|

|

|

|

|

|

City, Town or Post Office |

State |

ZIP Code |

|

Daytime Phone (with area code) |

AZ Transaction Privilege Tax License No. |

||

|

|

|

|

|

|

|

|

2. APPOINTEE INFORMATION |

|

|

|

|

2nd APPOINTEE INFORMATION (if applicable) |

|

|

Name |

|

|

|

|

Name |

|

|

|

|

|

|

||||

Current Address (if different from taxpayer’s address above) |

Apt./Suite |

Current Address (if different from taxpayer’s address above) |

Apt./Suite |

||||

|

|

|

|

|

|

|

|

City, Town or Post Office |

State |

ZIP Code |

|

|

City, Town or Post Office |

State ZIP Code |

|

|

|

|

|

|

|

|

|

Daytime Phone (with area code) |

|

|

|

|

Daytime Phone (with area code) |

|

|

|

|

|

|

|

|

|

|

Social Security, ITIN, or Other ID No. |

Type |

|

|

|

Social Security, ITIN, or Other ID No. Type |

|

|

|

| |

|

|

|

|

| |

|

3.TAX MATTERS: The appointee is authorized to receive confidential information for the tax matters listed below.

|

TAX TYPE |

YEAR(S) OR PERIOD(S) |

TYPE OF RETURN/OWNERSHIP |

|

||

|

Income Tax |

|

|

|

Corporation |

|

|

|

Individual |

|

|

||

|

|

|

Partnership |

|

||

Transaction Privilege |

|

Individual/Sole Proprietorship |

Partnership Corporation |

Trust |

||

|

and Use Tax |

|

Limited Liability Company |

Limited Liability Partnership |

Estate |

|

Withholding Tax |

|

|

|

|

|

|

|

|

|

|

|

||

Other (e.g., Luxury Tax): |

|

Specify type of return(s)/ownership: |

|

|

||

|

|

|

|

|

|

|

4.NO REVOCATION OF EARLIER AUTHORIZATION(S)

This Disclosure Authorization Form does not revoke any prior Power of Attorney or other authorization forms on file with the department.

5.SIGNATURE OF OR FOR TAXPAYER

I hereby certify that the Arizona Department of Revenue is authorized to release any and all confidential information concerning the Taxpayer(s). By signing this form, I certify that I have the authority, within the meaning of A.R.S.

By checking this box and signing below I certify under penalty of perjury that I am an officer of the above mentioned corporation(s) and that I am a principal officer, as defined in A.R.S.

________________________________________________ |

_______________________________________________ |

||

SIGNATURE |

DATE |

SIGNATURE |

DATE |

________________________________________________ |

_______________________________________________ |

||

PRINT NAME |

|

PRINT NAME |

|

________________________________________________ |

_______________________________________________ |

||

TITLE |

|

TITLE |

|

ADOR 10955 (8/18)

File Properties

| Fact Name | Description |

|---|---|

| Form Title | Arizona Form 285B Disclosure Authorization Form |

| Purpose | Authorizes the release of confidential taxpayer information to named appointee(s). |

| Power of Representation | Does not grant powers of representation to the appointee(s). |

| Required Signature | Must be signed in Section 5 by the taxpayer or a certified agent. |

| Governing Law | A.R.S. §42-2003(A) for authorization execution, A.R.S. §42-1127(B)(2) for legalities concerning fraudulent documents. |

| Earliest Revocation Policy | Does not revoke any prior Power of Attorney or other authorization forms. |

| Tax Matters Covered | Includes Income Tax, Transaction Privilege and Use Tax, Withholding Tax, and others specified by the taxpayer. |

| Penalty for Fraud | Presenting false information is a class 5 felony under A.R.S. §42-1127(B)(2). |

Instructions on Writing Arizona 285

Filling out the Arizona Form 285B, also known as the Disclosure Authorization Form, is a necessary step to authorize the Arizona Department of Revenue to release confidential tax information to a designated appointee. It's important to complete this form correctly to ensure that your appointee receives the information they need without any unnecessary delays. Remember, this form does not serve as a power of attorney or grant any representation powers. Here's how to fill it out properly:

- Section 1: Taxpayer Information

- Start by entering the taxpayer's name. This could be an individual or a business entity.

- Provide the Social Security Number (SSN) or the Individual Taxpayer Identification Number (ITIN) of the taxpayer. If this form is for a married couple or a business, include the spouse’s or co-owner's name and SSN/ITIN if applicable.

- Fill in the current address of the taxpayer, including the apartment or suite number if there is one.

- If the taxpayer is a business, enter the Employer Identification Number (EIN).

- Include the city, state, and ZIP code for the taxpayer’s address.

- Provide a daytime phone number, including the area code, where the taxpayer can be reached.

- If applicable, enter the Arizona Transaction Privilege Tax License Number.

- Section 2: Appointee Information

- Enter the name of the appointee authorized to receive the tax information. If there are two appointees, fill out the information for the second appointee in the area provided.

- For each appointee, if the current address is different from the taxpayer’s, enter it along with the apartment or suite number.

- Provide the city, state, and ZIP code for each appointee.

- Include a daytime phone number for each appointee.

- Enter the Social Security Number, ITIN, or Other ID Number for each appointee and specify the type of ID provided.

- Section 3: Tax Matters

- Check the box next to the tax type(s) for which the appointee is authorized to receive information.

- Specify the year(s) or period(s) and the type of return/ownership for each selected tax type.

- Section 4: No Revocation

- Acknowledge that completing this form does not revoke any prior Power of Attorney or other authorization forms on file with the department.

- Section 5: Signature

- The taxpayer (or an authorized representative) must sign and date the form, certifying that the Arizona Department of Revenue is authorized to release the specified confidential information.

- If the taxpayer is a corporation, check the box indicating that the signer is an officer of the corporation and is authorized to execute this form on behalf of the corporation.

- Print the name and title of the person signing the form.

After completing the form, review it carefully to ensure all information is accurate and complete. Then, submit the form as directed by the Arizona Department of Revenue. Proper completion and submission of this form facilitate the smooth processing of your request to share confidential tax information with your appointed representative(s).

Listed Questions and Answers

What is the Arizona Form 285B?

Arizona Form 285B, also known as the Disclosure Authorization Form, allows the Arizona Department of Revenue to share confidential taxpayer information with designated individuals, referred to as appointees. However, it's crucial to understand that this form does not function as a power of attorney, meaning it does not grant the appointee any right to represent the taxpayer in tax matters. It specifically authorizes the department to release information for the tax types and periods indicated on the form by the taxpayer.

Who needs to sign the Arizona Form 285B?

The taxpayer, whose information is to be disclosed, must sign the form. This act of signing confirms that the individual authorizes the Arizona Department of Revenue to release their confidential information to the specified appointee(s). It's also a declaration by the taxpayer that they have the legal right, per A.R.S. §42-2003(A), to grant this authorization. If the taxpayer represents a corporation, the individual signing on behalf of the corporation further certifies under penalty of perjury to be a principal officer of said corporation.

Can more than one appointee be designated on the Arizona Form 285B?

Yes, the form allows for the designation of more than one appointee. Taxpayers can fill out information for a second appointee in the designated section if they want another person to also have access to their confidential tax information. This flexibility ensures that taxpayers can have multiple trusted individuals authorized to receive important tax information, if necessary.

What tax types and periods can be specified on the Arizona Form 285B?

The taxpayer can specify a range of tax types and periods for which the appointee(s) can receive information. These tax types include, but are not limited to, Income Tax, Corporation, Individual, Partnership, Fiduciary-Estate/Trust, Transaction Privilege and Use Tax, Withholding Tax, and others such as Luxury Tax. Taxpayers can also indicate specific years or periods relevant to each tax type, ensuring that the authorization is tailored to their precise needs.

Does completing the Arizona Form 285B revoke previous authorizations?

No, filing this form does not revoke any previously filed Power of Attorney (POA) or other authorization forms. The Form 285B is designed solely to authorize the release of information without affecting any existing representation rights a taxpayer may have previously established through other forms. Taxpayers wishing to change or revoke existing authorizations must follow a separate process for each specific authorization.

What are the penalties for falsely signing the Arizona Form 285B?

Signing the Arizona Form 285B under false pretenses is considered a serious offense. Specifically, knowingly preparing or presenting a document that is fraudulent or false constitutes a class 5 felony, according to A.R.S. §42-1127(B)(2). This underscores the importance of providing accurate and truthful information when completing and signing the form, reflecting the legal commitment involved in the authorization process.

Common mistakes

Filling out the Arizona Form 285B, a Disclosure Authorization Form, involves providing the Arizona Department of Revenue with the requisite information to authorize the release of confidential tax information. However, mistakes can significantly impact the effectiveness and validity of the form. Here are nine common errors people make when completing this document:

- Incomplete Taxpayer Information: One of the most common errors is not fully completing the taxpayer information section. Every applicable field should be filled out, including taxpayer name, Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN), and current address. Missing information can delay processing.

- Incorrect Taxpayer Identifiers: Entering an incorrect SSN, ITIN, or Employer Identification Number (EIN) can lead to misidentification and improper handling of confidential information.

- Failure to Include Spouse’s Information: If married, providing spouse’s name and identifying number is crucial when the tax matter concerns joint filings. Overlooking this detail can restrict access to pertinent information.

- Appointee Details: People often neglect to fill out complete and accurate appointee information. This includes the appointee's name, address (if different from the taxpayer's), and identification number. Accurate details ensure that the correct individual is granted access to the specified information.

- Designating the Incorrect Tax Matters: Not clearly specifying the tax type, years, or periods for which disclosure is authorized can lead to confusion and the potential release of unintended information.

- Lack of Signature: The form requires a signature to be valid. Failing to sign the form results in its immediate rejection, as the signature certifies the requester’s authority to obtain the information.

- Not Checking the Perjury Statement Box: When the form is signed under penalty of perjury, particularly by officers of corporations, failing to check the appropriate box undermines the legal acknowledgment of the document's accuracy.

- Ignoring the No Revocation Clause: Mistakenly believing that submitting this form revokes previous authorizations is a common misunderstanding. This form does not nullify prior authorizations, and individuals must submit separate documentation for revocations.

- Incorrectly Assuming Power of Attorney: People often misconceive the form’s purpose, believing it grants the appointee power of attorney. This form strictly authorizes the release of information; it does not bestow any representation powers.

Avoiding these mistakes can streamline the process, ensuring the Arizona Department of Revenue can release the necessary information efficiently and accurately.

Documents used along the form

When handling various tax matters or interactions with the Arizona Department of Revenue, utilizing the Arizona 285 form is common practice. This form facilitates the authorized release of confidential tax information. However, this is often just one document in a broader suite of forms and documents that may be necessary for comprehensive tax management or legal representation. From granting broader powers of representation to requesting specific tax record types, the following documents typically accompany or complement the Arizona 285 form, helping individuals and businesses navigate their tax responsibilities with greater ease and precision.

- Power of Attorney (Form 285-POA): This form grants an individual or organization the authority to represent the taxpayer before the Arizona Department of Revenue, allowing them to make decisions and take actions regarding the taxpayer’s state tax matters.

- Transaction Privilege Tax Return: Used by businesses to report and pay the transaction privilege tax, often referred to as sales tax, which is collected from customers at the point of sale.

- Individual Income Tax Return Form (Form 140): Arizona residents use this form to file their annual state income tax returns, reporting their income, deductions, and credits to calculate their tax liability.

- Corporate Income Tax Return Form: This document is filed by corporations operating in Arizona to report their income, tax deductions, and credits, determining their state income tax liability.

- Withholding Tax Application: Employers use this application to register for withholding tax, allowing them to withhold state income tax from their employees' wages.

- Luxury Tax Return: Applicable to businesses that sell luxury items or services subject to additional taxes. This return is used to report and remit any luxury taxes owed.

- Application for Extension of Time to File: This form is used to request an extension of time to file the above tax returns, providing taxpayers additional time to gather necessary documentation and prepare their filings.

Navigating through these forms can be complex, prompting many individuals and organizations to seek guidance to ensure compliance and accuracy in their tax affairs. Each document serves a specific purpose in the broader context of state tax obligations and holds a unique place in the administrative toolkit for managing these responsibilities effectively. Understanding when and how to use these forms in conjunction with the Arizona 285 form is crucial for timely and efficient tax management.

Similar forms

The Arizona 285B form, known as the Disclosure Authorization Form, shares similarities with the IRS Form 2848, Power of Attorney and Declaration of Representative. Both forms serve to authorize an individual or entity to receive confidential tax information. However, while the Form 285B explicitly does not grant powers of representation or the ability to act on the taxpayer's behalf, the IRS Form 2848 does grant such powers, including, but not limited to, the authority to represent the taxpayer in front of the IRS, sign agreements, or make decisions regarding matters of tax.

Another document that resembles the Arizona 285B form is the IRS Form 8821, Tax Information Authorization. This form, like the Arizona 285B, allows the taxpayer to grant another party access to their confidential tax information without providing authority to represent the taxpayer before the IRS. The primary difference lies in the scope of authorization; where the IRS Form 8821 might be used to authorize the release of information to a broad range of entities for various reasons, the Arizona 285B is more narrowly focused on authorizing disclosure to specific appointees for tax matters.

The Arizona Form 321, Credit for Contributions to Qualifying Charitable Organizations, similarly involves taxpayer information but serves a different purpose. It is designed for taxpayers to claim tax credits for donations to certain charities. While it processes personal information and tax details akin to the Form 285B, its primary function is to facilitate tax credit claims rather than to authorize information disclosure.

The Arizona Form 202, Application for Extension of Time to File, also manages taxpayer information, including identification and contact details, similar to the initial sections of Form 285B. However, its purpose diverges significantly; it is specifically for requesting additional time to file a state tax return. The similarity lies in the administrative handling of taxpayer data, not in the authorization for information release.

The Transaction Privilege Tax Return form in Arizona, similar to the section of the 285B pertaining to the Transaction Privilege Tax, involves disclosing information about the taxpayer's business activities and liabilities. While both forms deal with Arizona tax matters, the privilege tax form is a filing requirement for businesses subject to the state's transaction privilege tax, focusing on reporting and payment of the tax, contrasting with the 285B's purpose of authorizing information disclosure.

Form 4506-T, Request for Transcript of Tax Return, shares a parallel with the Arizona 285B in that it also pertains to the release of tax information. Filed with the IRS, it requests a transcript of previously filed tax returns, which can include a variety of tax forms. Like the Arizona 285B, it requires taxpayer identification and signature for processing but serves the specific purpose of obtaining past tax return information from the federal government, not the state of Arizona.

Lastly, the Arizona Joint Tax Application for a Transaction Privilege, Use, and Severance Tax License is connected by its requirement for detailed taxpayer information to facilitate tax-related proceedings. Similar to parts of the Form 285B that deal with transaction privilege tax, this application gathers information to regulate tax liability for businesses within the state. However, its main goal is to obtain a license for operating a taxable entity in Arizona, diverging from the authorization focus of the 285B.

Dos and Don'ts

When completing the Arizona Form 285B, a disclosure authorization form, it's crucial to follow specific guidelines to ensure accurate and secure submission. Here are things you should and shouldn't do:

Do:

- Double-check the information: Ensure all details, including Taxpayer Name, Social Security Number or ITIN, and current address, are accurate to prevent processing delays.

- Clarify appointee details: If appointing someone, clearly provide their name, address, identification number, and specify their relationship or capacity accurately.

- Specify tax matters clearly: Detail the types of taxes and the years or periods they apply to. Ambiguity can lead to incomplete or incorrect disclosures.

- Understand the form's limitations: Acknowledge that this form does not grant power of attorney or revoke any previous authorizations.

- Sign and date the form: Your signature is essential, as it validates the document. Without it, the form won't be processed.

- Retain a copy for your records: Keeping a copy can help you track the process and maintain your records.

- Verify the appointee’s willingness and ability: Before you list someone as an appointee, ensure they are willing and able to handle this responsibility.

Don't:

- Omit relevant information: Leaving out necessary details may cause processing delays or result in the inability to fully comply with your request.

- Assume it grants legal authority: Remember, this form does not provide anyone with legal representation rights on your behalf.

- Use this form to revoke prior authorizations: This document cannot cancel or override previously granted permissions.

- Sign without reading: Understand every aspect of what you're authorizing, including the extent of detail the appointee(s) will have access to.

- Forget to check the relevant boxes: Especially the certification box in section 5 before signing. This oversight could invalidate your submission.

- Use outdated information: If any details have changed, especially contact information, ensure the form reflects the most current data.

- Fail to specify the tax type and period: Vague or incomplete tax information can lead to insufficient disclosure for your needs.

Misconceptions

Understanding the Arizona Form 285B, often referred to as the Disclosure Authorization Form, is crucial for accurate and lawful handling of tax-related matters. However, several misconceptions surround its use and implications. Let’s address some of these misunderstandings to ensure clarity and compliance.

Misconception #1: The Form Grants Power of Attorney. One common misunderstanding is that the Arizona Form 285B functions similarly to a Power of Attorney (POA). However, this form explicitly does not grant any powers of representation, meaning the appointee(s) cannot make decisions or file documents on behalf of the taxpayer; they can only receive confidential information.

Misconception #2: Signing Revokes Previous Authorizations. Another misconception is that by signing this form, any previous authorizations, including Powers of Attorney filed with the Arizona Department of Revenue, are revoked. The form states that it does not revoke any prior authorizations, so existing POAs or other disclosure permissions remain in effect.

Misconception #3: It Allows for Disclosure of All Tax Matters. While the form authorizes appointees to receive information, the scope is limited to the tax matters specifically listed in Section 3 of the form. It does not automatically include all types of taxes or periods unless explicitly stated.

Misconception #4: Any Individual can be an Appointee. Though the form allows for the designation of appointees, it implicitly requires that these appointees have a legitimate basis to receive the information. Merely knowing the taxpayer or being related does not necessarily qualify someone as an appointee without a proper reason related to the tax matters specified.

Misconception #5: The Form is Only for Individual Taxpayers. The language of the form accommodates not just individual taxpayers but also estates, trusts, corporations, and partnerships among others. This means the form is quite versatile and can be used across a broad spectrum of tax situations.

Misconception #6: Filing the Form is Compulsory for Tax Matters. Another misunderstanding is the belief that this form must be filed to address or manage any tax matters with the Arizona Department of Revenue. In reality, the form is optional and is specifically for authorizing the release of information, not for the broader engagement with the Department on tax matters.

Misconception #7: The Form is Effective Indefinitely. Lastly, there's a misconception that once signed, the authorization is permanent. The duration of the authorization is subject to the Department's policies and potentially state law but should not be assumed to be indefinite. Taxpayers and appointees should verify the current status of authorizations as needed.

Correcting these misunderstandings about the Arizona Form 285B can facilitate smoother interactions with the Arizona Department of Revenue, ensuring that both taxpayers and their appointees navigate tax matters with the correct permissions and expectations.

Key takeaways

Understanding the Arizona 285B Disclosure Authorization Form is crucial for accurate and legitimate communication of tax information. Here are key takeaways for effectively filling out and utilizing this form:

- The form explicitly does not function as a power of attorney. It simply authorizes the release of confidential tax information to designated appointees without granting them representation powers.

- Section 5 requires a mandatory signature to validate the form. This signature certifies that the individual has the authority to release tax-related information as per A.R.S. §42-2003(A).

- Taxpayer and appointee information must be filled out with precision, including current addresses and identification numbers, ensuring that the Arizona Department of Revenue can accurately process and direct the information.

- The form requires the designation of types of tax and specific periods or years for which information disclosure is authorized, making clear the scope of the authorization.

- Disclosure Authorization does not revoke any previous authorizations or Power of Attorney forms on file with the Department of Revenue, maintaining the validity of earlier submitted documents.

- It accommodates the inclusion of a second appointee, allowing for the authorization of two individuals to receive confidential tax information simultaneously.

- A check box is included for officers of a corporation to certify their authority under penalty of perjury, emphasizing the legal seriousness and implications of falsifying information on this form.

- By executing this form with truthful and complete information, individuals mitigate the risk of committing a class 5 felony related to presenting fraudulent documents as per A.R.S. §42-1127(B)(2).

Staying informed and vigilant when completing the Arizona 285B Disclosure Authorization Form can enhance the security and proper handling of sensitive tax information, underscoring the importance of thoroughness and honesty in the process.

Discover Common PDFs

Arizona Unclaimed Property - The Arizona 652 form plays a pivotal role in the state's efforts to prevent unclaimed property from remaining indefinitely with holders.

Paternity Test Arizona - The procedure outlined in this form includes understanding that either parent can challenge the acknowledgment under state law.