Fill in Your Arizona 5000 Form

The Arizona 5000 form plays a critical role in documenting transactions that are exempt from the state's Transaction Privilege Tax (TPT), ensuring that businesses can accurately apply for and claim necessary exemptions. This specialized form, governed by the Arizona Department of Revenue, enables purchasers to establish a clear basis for state and city tax deductions or exemptions across a variety of transaction types. From transactions with U.S. Government entities to those involving Native Americans or specific business-to-business purchases, the form covers various grounds, including sales of tangible personal property and certain services. It delineates strict guidelines for its use, explicitly stating when alternative forms, such as the 5000A for sale for resale or the 5000M for non-TPT licensed contractors, should be utilized instead. Each certificate must be filled out comprehensively by the purchaser and provided to the vendor at the time of sale, with the vendor responsible for retaining the certificate for either single transactions or for a duration specified within the document. Moreover, the form cautions against incomplete submissions, emphasizing that only fully completed certificates can be considered accepted in good faith. Additionally, it addresses potential penalties for misuse, highlighting the serious consequences of fraudulent claims, including monetary penalties and criminal charges. By catering to a broad spectrum of exemptions and underscoring the importance of proper documentation and adherence to guidelines, the Arizona 5000 form serves as an essential tool for businesses navigating the complexities of transaction privilege tax exemptions.

Document Preview

Arizona Form |

Transaction Privilege Tax Exemption Certificate |

|

5000 |

||

|

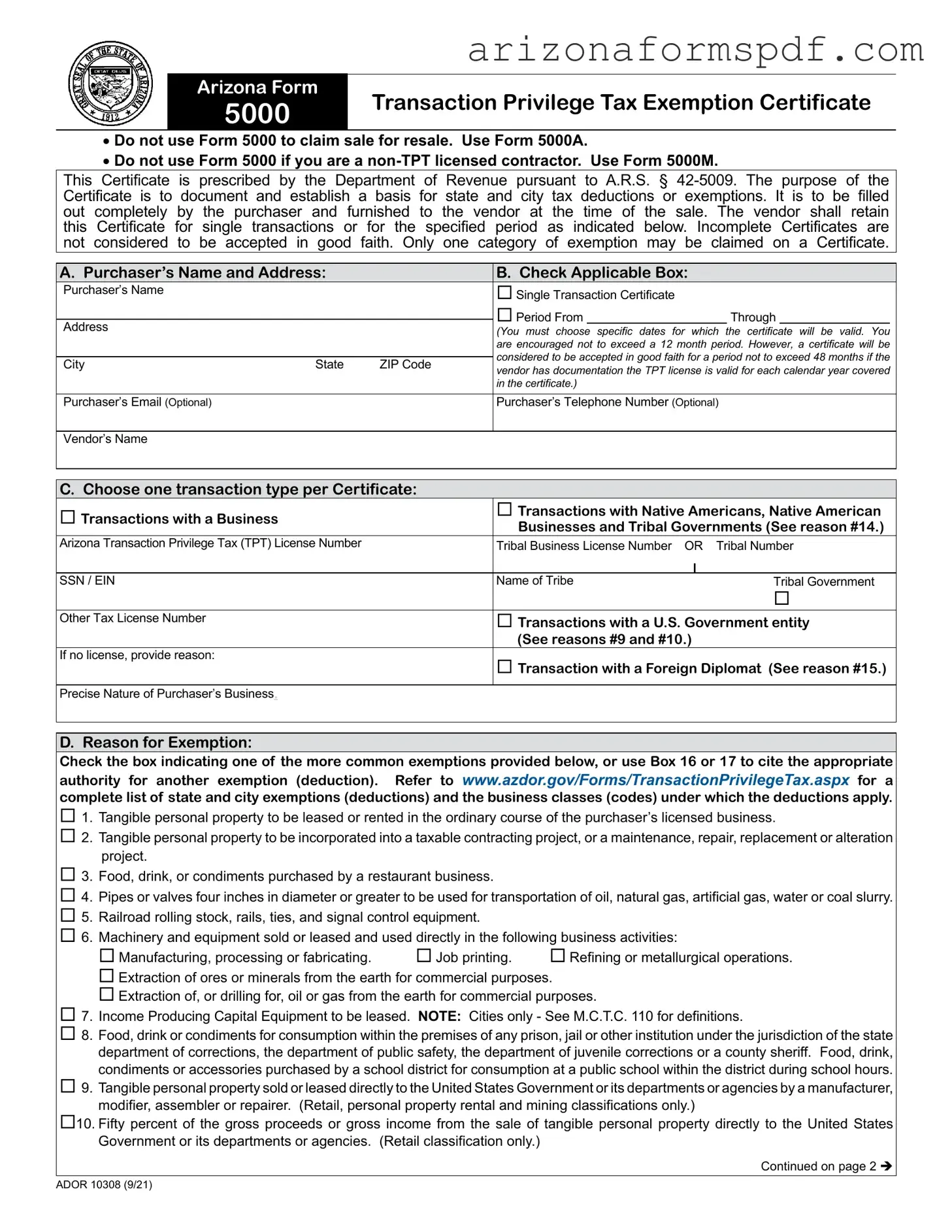

•Do not use Form 5000 to claim sale for resale. Use Form 5000A.

•Do not use Form 5000 if you are a

This Certificate is prescribed by the Department of Revenue pursuant to A.R.S. § |

||||||||||

Certificate is to document and establish a basis for |

state and city tax deductions or exemptions. It is to be filled |

|||||||||

out completely by the purchaser and furnished to |

the vendor at the time of |

the sale. The vendor shall retain |

||||||||

this Certificate for single transactions or |

for the specified period as indicated |

below. Incomplete Certificates are |

||||||||

not considered to be accepted in good faith. Only |

one category of exemption may be claimed on a Certificate. |

|||||||||

|

|

|

|

|

|

|

|

|

||

A. Purchaser’s Name and Address: |

|

|

B. Check Applicable Box: |

|||||||

Purchaser’s Name |

|

|

|

Single Transaction Certificate |

||||||

|

|

|

|

Period From |

|

|

|

Through |

|

|

Address |

|

|

|

|||||||

|

|

|

(You must choose specific |

dates for which the certificate will be valid. You |

||||||

|

|

|

|

are encouraged not to exceed a 12 month period. However, a certificate will be |

||||||

|

|

|

|

considered to be accepted in good faith for a period not to exceed 48 months if the |

||||||

City |

State |

ZIP Code |

|

|||||||

|

vendor has documentation the TPT license is valid for each calendar year covered |

|||||||||

|

|

|

|

|||||||

|

|

|

|

in the certificate.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Purchaser’s Email (Optional) |

|

|

|

Purchaser’s Telephone Number (Optional) |

||||||

|

|

|

|

|

|

|

|

|

|

|

Vendor’s Name |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

C. Choose one transaction type per Certificate: |

|

|

|

|

|

|

|

|

||

Transactions with a Business |

|

|

|

Transactions with Native Americans, Native American |

||||||

|

|

|

Businesses and Tribal Governments (See reason #14.) |

|||||||

|

|

|

|

|||||||

Arizona Transaction Privilege Tax (TPT) License Number |

|

|

Tribal Business License Number OR Tribal Number |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

SSN / EIN |

|

|

|

Name of Tribe |

|

|

Tribal Government |

|||

|

|

|

|

|

|

|

|

|

||

Other Tax License Number |

|

|

|

Transactions with a U.S. Government entity |

||||||

|

|

|

|

(See reasons #9 and #10.) |

||||||

If no license, provide reason: |

|

|

|

Transaction with a Foreign Diplomat (See reason #15.) |

||||||

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

Precise Nature of Purchaser’s Business. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D. Reason for Exemption:

Check the box indicating one of the more common exemptions provided below, or use Box 16 or 17 to cite the appropriate authority for another exemption (deduction). Refer to www.azdor.gov/Forms/TransactionPrivilegeTax.aspx for a complete list of state and city exemptions (deductions) and the business classes (codes) under which the deductions apply.

1. Tangible personal property to be leased or rented in the ordinary course of the purchaser’s licensed business.

2. Tangible personal property to be incorporated into a taxable contracting project, or a maintenance, repair, replacement or alteration project.

3. Food, drink, or condiments purchased by a restaurant business.

4. Pipes or valves four inches in diameter or greater to be used for transportation of oil, natural gas, artificial gas, water or coal slurry.

5. Railroad rolling stock, rails, ties, and signal control equipment.

6. Machinery and equipment sold or leased and used directly in the following business activities:

Manufacturing, processing or fabricating. |

Job printing. |

Refining or metallurgical operations. |

Extraction of ores or minerals from the earth for commercial purposes.

Extraction of, or drilling for, oil or gas from the earth for commercial purposes.

7. Income Producing Capital Equipment to be leased. NOTE: Cities only - See M.C.T.C. 110 for definitions.

8. Food, drink or condiments for consumption within the premises of any prison, jail or other institution under the jurisdiction of the state department of corrections, the department of public safety, the department of juvenile corrections or a county sheriff. Food, drink, condiments or accessories purchased by a school district for consumption at a public school within the district during school hours.

9. Tangible personal property sold or leased directly to the United States Government or its departments or agencies by a manufacturer, modifier, assembler or repairer. (Retail, personal property rental and mining classifications only.)

10. Fifty percent of the gross proceeds or gross income from the sale of tangible personal property directly to the United States Government or its departments or agencies. (Retail classification only.)

Continued on page 2

ADOR 10308 (9/21)

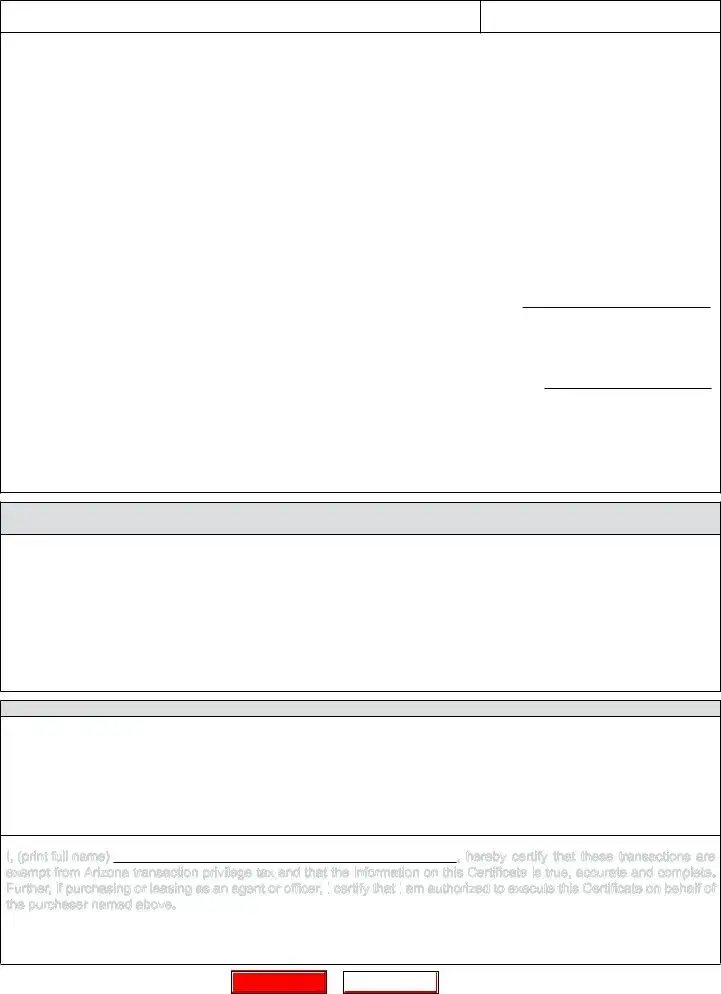

Your Name (as shown on page 1)

Arizona Transaction Privilege Tax License Number

11. Electricity, natural gas or liquefied petroleum gas sold to a qualified manufacturing or smelting business. A manufacturing or smelting business that claims this exemption authorizes the release by the vendor of the information required to be provided to the Department of Revenue pursuant to A.R.S. §

12. Electricity or natural gas to a business that operates an international operations center in this state and that is certified by the Arizona Commerce Authority. NOTE: Certification must be attached. (Utilities classification only.) (Not available for all Cities.)

13. Computer data center equipment sold to the owner, operator or qualified colocation tenant of a computer data center that is certified by the Arizona Commerce Authority pursuant to A.R.S. §

14. Sale or lease of tangible personal property to affiliated Native Americans if the order is placed from and delivered to the reservation. NOTE: The vendor shall retain adequate documentation to substantiate the transaction.

15. Foreign diplomat. NOTE: Limited to authorization on the U.S. Department of State Diplomatic Tax Exemption Card. The vendor shall retain a copy of the U.S. Department of State Diplomatic Tax Exemption Card and any other documentation issued by the U.S. Department of State. Motor vehicle purchases or leases must be

16.*Other Deduction: Cite the Arizona Revised Statutes authority for the deduction. A.R.S. §

Description:

17.*Other Cities Deduction: Cite the Model City Tax Code authority for the deduction. M.C.T.C. § Description:

*Refer to www.azdor.gov/TransactionPrivilegeTax(TPT)/RatesandDeductionCodes.aspx for a complete list of state and city exemptions (deductions) and the business classes (codes) under which the deductions apply.

E.Describe the tangible personal property or service purchased or leased and its use below. (Use additional pages if needed.)

F. Certification

A vendor that has reason to believe that this Certificate is not accurate or complete will not be relieved of the burden of proving entitlement to the exemption. A vendor that accepts a Certificate in good faith will be relieved of the burden of proof and the purchaser may be required to establish the accuracy of the claimed exemption. If the purchaser cannot establish the accuracy and completeness of the information provided in the Certificate, the purchaser is liable for an amount equal to the transaction privilege tax, penalty and interest which the vendor would have been required to pay if the vendor had not accepted the Certificate. Misuse of this Certificate will subject the purchaser to payment of the A.R.S. §

I, (print full name) |

, hereby certify that these transactions are |

exempt from Arizona transaction privilege tax and that the information on this Certificate is

on this Certificate is true, accurate and complete. Further, if

true, accurate and complete. Further, if purchasing or leasing as an agent or officer, I

purchasing or leasing as an agent or officer, I certify that I

certify that I am authorized to execute this Certificate on behalf of the purchaser named above.

am authorized to execute this Certificate on behalf of the purchaser named above.

SIGNATURE OF PURCHASER |

|

DATE |

|

TITLE |

ADOR 10308 (9/21)

Page 2 of 2

Print Form

Reset Form

File Properties

| Fact Name | Description |

|---|---|

| Governing Law | The Arizona Form 5000 is governed by Arizona Revised Statutes § 42-5009, which prescribes the use and requirements of the Transaction Privilege Tax Exemption Certificate. |

| Purpose | The purpose of the Arizona Form 5000 is to document and establish a basis for state and city tax deductions or exemptions for eligible transactions. |

| Proper Use | Form 5000 should not be used for claiming a sale for resale, which requires Form 5000A, or by non-TPT licensed contractors, who should use Form 5000M instead. |

| Validity and Good Faith Acceptance | The Certificate must be fully completed by the purchaser and provided to the vendor at the time of sale. It is considered to be accepted in good faith for a period not to exceed 48 months, given the vendor has documentation the TPT license is valid for each calendar year covered. |

Instructions on Writing Arizona 5000

Completing the Arizona Form 5000 requires attention to detail and understanding of your specific transaction to ensure accurate filing. This document serves a critical role in establishing a basis for state and city tax deductions or exemptions for various transactions. Below, you'll find a straightforward guide to help you navigate the process effortlessly.

- Start by entering the Purchaser’s Name and Address in Section A, ensuring the information matches your official documents.

- Under Section B, Check the Applicable Box to indicate whether you're using this certificate for a single transaction or specifying a period. Remember, a certificate for a period should not exceed 48 months.

- In Section C, Choose one transaction type per Certificate from the provided options.

- For Section D, Reason for Exemption, carefully review the list of common exemptions. Check the box next to the exemption that applies to your situation. If your exemption isn't listed, use Box 16 or 17 to cite the appropriate authority for your specific exemption or deduction.

- In the space provided in Section E, describe the tangible personal property or service purchased or leased and its intended use. Attach additional pages if necessary.

- The Certification Section F is crucial. After reading, sign at the bottom to certify the accuracy and completeness of the information provided. This section emphasizes the responsibility of the purchaser in case of inaccuracies.

- Provide the purchaser's signature, date, and title to finalize the certificate.

Upon completion, furnish this Certificate to the vendor at the time of the sale. It is important for the vendor to retain this Certificate for their records, as it validates the transaction's exemption from Arizona transaction privilege tax under the law. Misuse or inaccurate completion of this document may lead to penalties, interest charges, or criminal liabilities. Approach this document with the seriousness and accuracy it demands.

Listed Questions and Answers

What is the Arizona Form 5000, and when should it be used?

Arizona Form 5000, known as the Transaction Privilege Tax Exemption Certificate, is a document designed to help businesses document and establish a basis for claiming exemptions from the state and city transaction privilege tax (TPT), often referred to as a sales tax. Businesses should use this form when they are making purchases that they believe are exempt from TPT under Arizona law. This might include purchases of goods that will be resold, machinery for manufacturing, or goods purchased by a government entity. Importantly, the form must be filled out completely and given to the vendor at the time of the sale. Each exemption claim must be substantiated with specific reasoning laid out in the form, and only one category of exemption can be claimed per certificate.

Can Form 5000 be used for all types of TPT exemptions?

No, Form 5000 cannot be used for all types of exemptions. Specifically, it should not be used if the purchase is for resale - in that case, Form 5000A is required. Additionally, non-TPT licensed contractors must use Form 5000M instead. This delineation ensures that the right documentation is used for the corresponding exemption claims, allowing for clearer tax and legal compliance for different types of transactions.

How long is the exemption certificate valid?

The validity of the exemption certificate can be chosen by the purchaser but is encouraged not to exceed a 12-month period. However, in situations where longer coverage is necessary, the certificate can be accepted in good faith for a period not to exceed 48 months. This extension requires the vendor to have documentation proving the purchaser's TPT license is valid for each calendar year covered by the certificate. This flexibility allows businesses to manage and plan their exemption claims more efficiently over a specified period.

What happens if the Form 5000 is filled out incompletely?

An incomplete Form 5000 is not accepted in good faith, which implies that the vendor will not recognize the purchase as exempt from the TPT. Completeness of the certificate is crucial for its acceptance, as it assures the vendor – and by extension, the Arizona Department of Revenue – that due diligence has been exercised in claiming the tax exemption. Therefore, if the form is incomplete, the purchaser cannot benefit from the exemption, and they might end up being liable for the transaction privilege tax, additional penalties, and interest. Moreover, misuse or fraudulent claiming of exemptions can lead to criminal penalties, emphasizing the importance of accuracy and completeness when filling out the form.

Common mistakes

Filling out forms can be tricky, and the Arizona Form Transaction Privilege Tax Exemption Certificate 5000 is no exception. There are common pitfalls that many people stumble into when attempting to navigate these waters. To help steer clear of these, let’s pinpoint five critical mistakes often made during the completion process.

- Using Form 5000 for Inappropriate Claims: A frequent oversight is the attempt to use Form 5000 for claims that it's not designed for, such as sales for resale, which should be processed through Form 5000A, or for non-TPT licensed contractors, who need to use Form 5000M. Each form has its purpose and mixing them up can invalidate the exemption claim.

- Incomplete Certificates: One of the biggest hurdles to getting your exemption accepted in good faith is submitting an incomplete certificate. Every section of the form that applies to your situation needs to be filled out thoroughly. Incomplete submissions can lead to delays or outright rejection.

- Choosing More Than One Exemption Category: The form allows for only one category of exemption per certificate. However, a common misstep is attempting to claim multiple categories on a single form. This mistake can cloud the intended exemption, causing confusion and potential disqualification.

- Ignoring Date Validity: The period for which the certificate is valid must be clearly indicated, without exceeding the 12-month recommendation. Understandably, though, allowances are made for durations not exceeding 48 months, provided there is verifiable documentation of the TPT license’s validity each calendar year. Oversights in this area might lead to complications in the exemption’s acceptance.

- Failure to Provide Adequate Documentation for Certain Exemptions: Specific exemptions, like those involving transactions with Native American entities or foreign diplomats, require additional documentation. Neglecting to attach such crucial evidence can render the exemption claim invalid.

Making sure to avoid these common errors can greatly enhance the likelihood of successfully claiming your exemption without delay. Whether you’re a new applicant or seasoned in handling tax exemption forms, paying attention to the finer details outlined above can make all the difference in the successful submission of your Arizona Form 5000.

Documents used along the form

When navigating the complexities of the Arizona transaction privilege tax (TPT), understanding the additional documentation that can be required or beneficial alongside the Arizona 5000 form is crucial. This form, essential for documenting state and city tax exemptions, often works in conjunction with other forms and documents to provide a comprehensive overview of a business's tax responsibilities and exemptions. Here's a look at seven other forms and documents frequently used alongside the Arizona 5000 form:

- Form 5000A: This form is specifically used for claiming a sale for resale exemption. Unlike the 5000 form, which covers a broad range of exemptions, the 5000A is focused on resellers who buy goods only to sell them again.

- Form 5000M: Non-TPT licensed contractors must use this form to document their purchases exempt from the transaction privilege tax. It's tailored to the unique circumstances of contractors operating without a TPT license.

- Form 5000HC: This is used for documenting exemptions on healthcare-related purchases. It covers medical and pharmaceutical supplies that are exempt from TPT under Arizona law.

- Transaction Privilege Tax Return: While not a form for exemptions, this return is where a business reports its taxable sales and calculates the tax owed, making it a critical document for any business subject to TPT.

- Exemption Certificate for Native Americans (Form 5000NA): This certificate is required for transactions involving Native Americans or Native American businesses, providing documentation to substantiate tax exemption claims based on tribal sovereignty.

- Annual Business License Renewal: Although it's not a TPT-specific form, maintaining an up-to-date business license is vital for claiming exemptions. In many cases, the validity of forms like the 5000 and 5000A is contingent upon the business's licensure status.

- TPT Exemption Certificate for Government Purchases (Form 5000G): Similar to the 5000 form, this document is used specifically for transactions with government entities, documenting the tax-exempt status of goods and services sold to various levels of government.

Together, these forms and documents form a toolkit for businesses to navigate Arizona's transaction privilege tax landscape effectively. Keeping accurate and current documentation is key to maintaining compliance and ensuring that a business takes full advantage of applicable tax exemptions. Handling these obligations with diligence will safeguard against potential disputes or liabilities arising from tax exemption claims.

Similar forms

The Arizona Form 5000, focusing on Transaction Privilege Tax Exemption, bears resemblances to other tax exemption or resale documents utilized across various states due to its purpose in documenting tax-exempt transactions. Similar forms, such as the Texas Sales and Use Tax Resale Certificate, also require buyers to declare the purpose of their tax-exempt purchases, ensuring that vendors have the necessary documentation to report to state revenue departments. Both forms help prevent tax evasion by providing detailed requirements for the type of exempt transactions, guiding vendors and purchasers in complying with tax laws.

The California Resale Certificate is another document resembling the Arizona Form 5000 in its aim to facilitate tax-exempt purchases for resale. Like the Form 5000, it mandates that purchasers provide specific details about the business and the nature of the tax-exempt transaction. These certificates play a critical role in the retail sector, ensuring that sales tax is only applied to end consumers, and not at various points of product distribution and resale.

New York's Resale Certificate functions similarly to Arizona's Form 5000, allowing businesses to purchase goods tax-free when those goods are intended for resale. Both documents require purchasers to furnish their business type and the reason for the exemption. They clearly outline the responsibilities of the purchaser and the vendor, emphasizing the importance of maintaining accurate records for tax audits.

The Florida Annual Resale Certificate for Sales Tax shares commonalities with the Arizona Form 5000 by allowing businesses to make tax-exempt purchases for resale. Each state's regulations bespoke the procedure for using such certificates, highlighting the need for interstate businesses to be aware of varying requirements. Both forms are integral in ensuring that taxes are accurately collected and reported at the point of final sale to the consumer.

Similar to the Arizona Form 5000, the Illinois Certificate of Resale is designed for transactions where goods are bought for resale. Both certificates necessitate detailed information about the purchaser and the intended exemption. They serve a pivotal function in commerce by distinguishing between taxable retail sales and tax-exempt wholesale transactions.

In addition to specific resale certificates, there are broader exemption certificates like the Multistate Tax Commission’s Uniform Sales & Use Tax Certificate. This multijurisdictional form covers exemptions beyond resale, such as manufacturing or nonprofit exceptions, much like the varied exemption reasons listed on Arizona's Form 5000. These forms are invaluable tools for businesses operating in multiple states, streamlining the process of tax exemption documentation.

For transactions involving government entities, forms like the Governmental Agency Exemption Certificate illustrate similarities to Arizona's Form 5000, which provides exemptions for transactions with U.S. Government entities. Both documents are essential for accurately documenting tax-exempt sales to government bodies, ensuring compliance with specific tax exemption statutes.

Arizona Form 5000M, specifically for non-TPT licensed contractors, also shares a foundational purpose with Form 5000, yet it caters to a niche category of transactions. The existence of both forms underscores Arizona’s effort to accommodate a wide array of tax-exempt transactions, tailoring documentation requirements to various business scenarios.

The Streamlined Sales Tax Agreement’s Exemption Certificate is another document akin to the Arizona Form 5000, designed to facilitate tax-exempt purchases across participating states. While aimed at simplifying the tax exemption process for businesses, it similarly demands detailed information from the purchaser about the nature of the exemption, underscoring the uniform need for precise documentation in tax-exempt sales.

The Arizona Form 5000A, intended for claiming sales for resale, operates in conjunction with the general exemption certificate (Form 5000) by providing a more focused avenue for a specific exemption type. This division of exemption scenarios into separate forms helps clarify the documentation process for both vendors and purchasers, ensuring the appropriate application of tax laws.

Dos and Don'ts

When completing the Arizona Form 5000 Transaction Privilege Tax Exemption Certificate, attention to detail is crucial. Below are essential guidelines to ensure the process is handled correctly, including what should and should not be done.

- Do make sure to use Form 5000 for the correct purpose. It is designed to document and establish a basis for state and city tax deductions or exemptions, not for sale for resale transactions, which require Form 5000A.

- Do not use Form 5000 if you are a non-TPT licensed contractor. In such cases, Form 5000M is the correct document to use.

- Do fill out the form completely and accurately. Incomplete forms are not considered to be provided in good faith and could lead to disqualification of the exemption claim.

- Do not claim more than one category of exemption on a single Certificate. Each exemption claim requires a separate form.

- Do choose specific dates if opting for a period certificate. While you are encouraged not to exceed a 12-month period, a certificate can be considered valid for no more than 48 months, provided the vendor has documentation that the TPT license is valid for each calendar year covered.

- Do not misuse the Certificate. Misuse can lead to the purchaser being liable for the transaction privilege tax, penalty, and interest, and willful misuse can result in criminal penalties.

Do ensure that the reason for exemption is clearly marked and corresponds with the reasons listed on the form. If claiming an exemption not listed, cite the appropriate Arizona Revised Statutes or Model City Tax Code authority in the provided space.- Do not sign the form without the authority to do so. By signing the form, you are certifying that all the information provided is true, accurate, and complete, and that you are authorized to execute the Certificate on behalf of the purchaser.

Following these guidelines will help ensure the Arizona Form 5000 is filled out correctly and efficiently, leading to a smoother process for claiming tax deductions or exemptions.

Misconceptions

Understanding the Arizona Form 5000, or the Transaction Privilege Tax Exemption Certificate, is crucial for both vendors and purchasers involved in taxable transactions. However, misconceptions about this form can lead to mishandling tax exemptions, potentially resulting in financial penalties and complications. Let's clarify some common misunderstandings:

- Misconception #1: Form 5000 can be used for all types of tax exemptions.

- Misconception #2: A vendor does not need to retain the Certificate for verification.

- Misconception #3: Multiple exemption categories can be claimed on a single Certificate.

- Misconception #4: Incomplete Certificates are acceptable as long as the essential information is provided.

- Misconception #5: The form's validity is restricted to a short term, typically 12 months.

- Misconception #6: Any purchase made by qualifying organizations, like schools or government entities, is automatically exempt.

Contrary to this belief, Form 5000 is not a one-size-fits-all solution for claiming tax exemptions. Specific exemptions, such as sales for resale, require different forms, like Form 5000A. Similarly, non-TPT licensed contractors must use Form 5000M instead.

Actually, vendors are required to retain this Certificate to substantiate the tax exemption of a transaction. It serves as a record that can be verified during audits or reviews by the tax authorities.

Each Certificate limits the claim to one category of exemption. Trying to claim multiple categories on a single Certificate can invalidate the exemption claim, as it goes against the prescribed guidelines.

In reality, completeness is crucial for the acceptance of the Certificate in good faith. Missing information can lead to the rejection of the exemption claim, emphasizing the necessity for thoroughness when filling out the form.

While a 12-month validity period is encouraged, a Certificate can remain valid for up to 48 months if the vendor can document the purchaser’s TPT license validity for each year within this period. This exception allows for longer-term exemptions under specific conditions.

Exemptions are not universally applicable just by virtue of the purchaser's status. The nature of the purchase and its use are significant factors in determining eligibility for tax exemptions. For instance, specific exemptions apply to food consumed within certain institutions or to items sold directly to the U.S. Government.

Recognizing these misconceptions and understanding the correct use of Arizona Form 5000 is essential for both purchasers and vendors to ensure compliance with tax exemption regulations. Accurate completion and proper handling of this form help in avoiding unnecessary liabilities and ensuring smooth transactions free from tax-related complications.

Key takeaways

Understanding how to correctly complete and utilize the Arizona Form 500O for Transaction Privilege Tax Exemption is critical. Here are ten key takeaways that individuals and businesses should be aware of:

- The Form 5000 is specifically designed to document and establish a basis for state and city tax deductions or exemptions. It is not to be used for claiming sale for resale, for which Form 5000A is appropriate.

- Purchasers who are non-TPT licensed contractors should not use Form 5000, but should instead use Form 5000M.

- For a valid exemption claim, the purchaser must fill out the Certificate completely and furnish it to the vendor at the time of sale. Incomplete Certificates cannot be accepted in good faith.

- The form allows for the specification of a period for which the certificate will be valid, not exceeding a 12 month period. However, under certain conditions, a period not exceeding 48 months may be accepted if the vendor has documented proof of a valid TPT license for each calendar year covered.

- A Certificate can only claim one category of exemption. Selecting the appropriate category is crucial for the Certificate to be considered valid.

- A variety of exemptions are available, including but not limited to, purchases by restaurants, leases, and sales to the U.S. Government or its agencies. Each exemption has specific qualifications and requirements.

- If the exemption claimed does not fit within the listed common exemptions, purchasers can reference the Arizona Revised Statutes or the Model City Tax Code in the provided sections for other deductions.

- For transactions with Native Americans, U.S. Government entities, or foreign diplomats, specific documentation and verification practices are required to substantiate the transaction.

- The vendor holds the responsibility to verify the accuracy and completeness of the Certificate. If accepted in good faith, the burden of proof shifts away from the vendor to the purchaser, should questions arise.

- Misuse of the Certificate, whether intentional or not, could result in the purchaser being liable for the equivalent amount of transaction privilege tax, including any penalties and interest. Willful misuse carries the risk of felony charges.

These takeaways underscore the importance of diligence and accuracy in the use of Arizona's Form 5000 for Transaction Privilege Tax Exemption. Compliance with the form's requirements not only ensures adherence to tax regulations but also protects both the purchaser and vendor from potential legal and financial liabilities.

Discover Common PDFs

Arizona 676 - Promotes legal and orderly registration of watercraft while recognizing lien holders’ rights.

Arizona Repo Affidavit - Ensures a lienholder's authority to repossess a defaulted vehicle in Arizona is well-documented along with any sale of the vehicle, including accurate mileage reporting.