Fill in Your Arizona 74 Form

In the realm of estate management and taxation within Arizona, the Arizona Form 74 stands out as a pivotal document, designed to streamline the reporting process for personal representatives of decedents. Tasked with the meticulous job of reporting to the Estate Tax Unit of the Arizona Department of Revenue, this form encapsulates a comprehensive summary pertaining to the estate's federal identification number, decedent information including social security number and date of death, along with a detailed account of the estate's assets segmented into real estate, bank deposits, securities, and other tangible assets. The necessity to attach a death certificate for original reports underscores the form's role in formalizing estate proceedings within the state's jurisdiction. Furthermore, the optionality between Original and Amended reports facilitates ongoing accuracy in the estate’s representation. With sections dedicated to the summary of the estate, requested documents including waivers for estate tax, and a thorough breakdown of estate assets, the Arizona 74 form serves as a critical conduit ensuring that estate valuation is properly accounted for, potentially necessitating the filing of a federal estate tax return. Offering clear instructions for personal representatives, the form not only aides in adhering to Arizona's tax laws but also simplifies the complex process of estate reporting, making it an indispensable tool for those navigating the intricacies of estate administration post-decease.

Document Preview

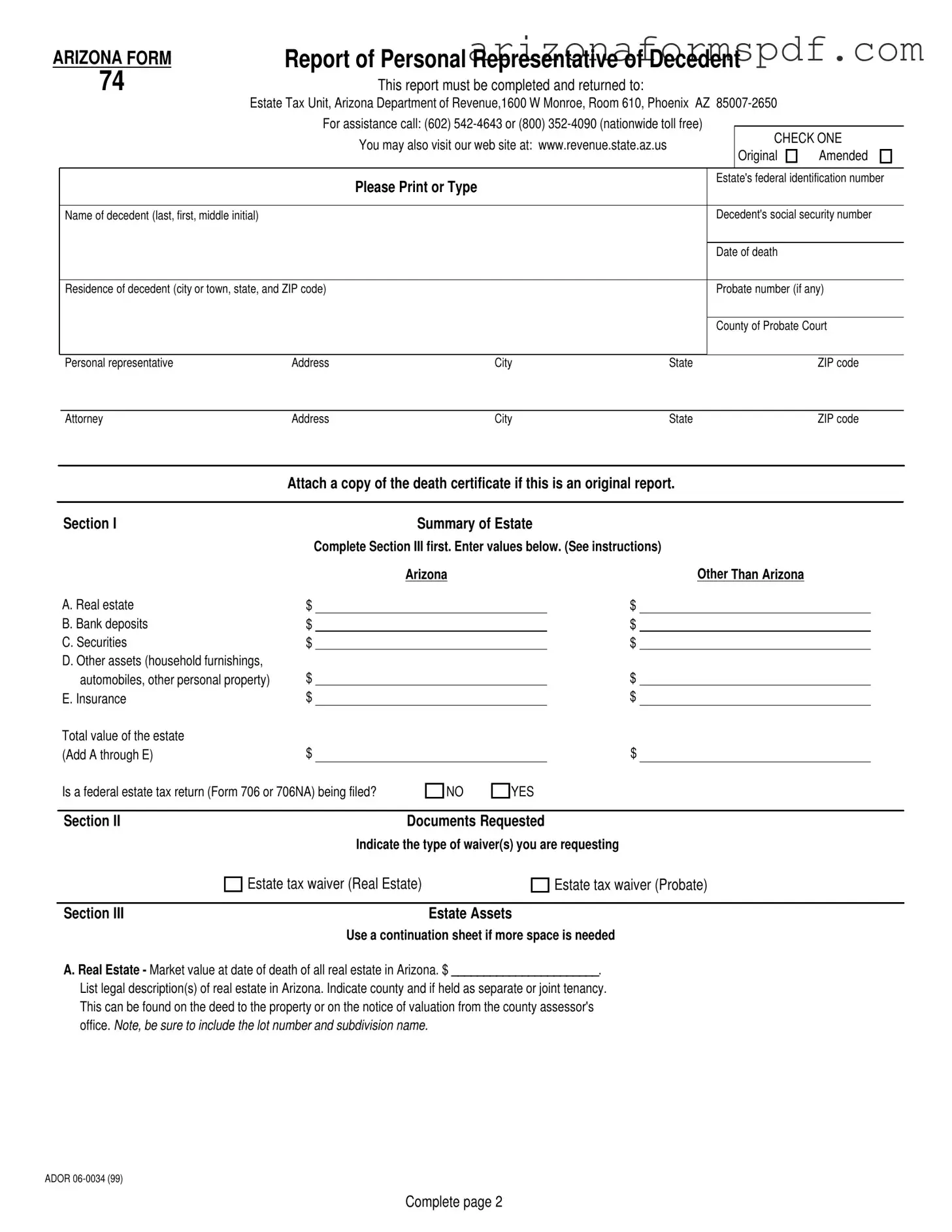

ARIZONA FORM |

Report of Personal Representative of Decedent |

|

|

||||||||

74 |

|

|

This report must be completed and returned to: |

|

|

|

|

|

|||

|

Estate Tax Unit, Arizona Department of Revenue,1600 W Monroe, Room 610, Phoenix AZ |

|

|

||||||||

|

|

|

For assistance call: (602) |

|

|

|

|||||

|

|

|

|

You may also visit our web site at: www.revenue.state.az.us |

|

|

CHECK ONE |

||||

|

|

|

|

|

|

Original |

Amended |

||||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Please Print or Type |

|

|

|

Estate's federal identification number |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name of decedent (last, first, middle initial) |

|

|

|

|

|

|

Decedent's social security number |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Date of death |

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

Residence of decedent (city or town, state, and ZIP code) |

|

|

|

|

Probate number (if any) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

County of Probate Court |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Personal representative |

Address |

City |

|

State |

|

|

|

ZIP code |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Attorney |

Address |

City |

|

State |

|

|

|

ZIP code |

||

|

|

|

|

|

|

|

|

|

|

||

|

|

Attach a copy of the death certificate if this is an original report. |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Section I |

|

|

Summary of Estate |

|

|

|

|

|

|

|

|

|

Complete Section III first. Enter values below. (See instructions) |

|

|

|

|

|

||||

|

|

|

|

Arizona |

|

|

Other Than Arizona |

|

|

||

|

A. Real estate |

$ |

|

|

$ |

|

|

|

|

|

|

|

B. Bank deposits |

$ |

|

|

$ |

|

|

|

|

|

|

|

C. Securities |

$ |

|

|

$ |

|

|

|

|

|

|

|

D. Other assets (household furnishings, |

|

|

|

|

|

|

|

|

|

|

|

automobiles, other personal property) |

$ |

|

|

$ |

|

|

|

|

|

|

|

E. Insurance |

$ |

|

|

$ |

|

|

|

|

|

|

|

Total value of the estate |

|

|

|

|

|

|

|

|

|

|

|

(Add A through E) |

$ |

|

|

$ |

|

|

|

|

|

|

Is a federal estate tax return (Form 706 or 706NA) being filed?

NO

YES

Section II |

Documents Requested |

Indicate the type of waiver(s) you are requesting

Estate tax waiver (Real Estate)

Estate tax waiver (Probate)

Section III |

Estate Assets |

|

Use a continuation sheet if more space is needed |

A. Real Estate - Market value at date of death of all real estate in Arizona. $ _______________________.

List legal description(s) of real estate in Arizona. Indicate county and if held as separate or joint tenancy. This can be found on the deed to the property or on the notice of valuation from the county assessor's

office. NOTE, BE SURE TO INCLUDE THE LOT NUMBER AND SUBDIVISION NAME.

ADOR

Complete page 2

Form 74 Page 2

B. Bank Deposits - List accounts in financial institutions.

Name of bank or other institution |

Type of account |

Balance at date of death |

|

|

|

Total Value |

$ __________________ |

|

|

|

|

|

C. Securities - List all stocks, bonds, and other securities that were owned by the decedent. |

|

|

||

Name of company |

Number of shares |

Value at date of death |

||

Total Value |

$ __________________ |

D. Other Assets - List other assets (household furnishings, motor vehicles, and other personal property).

Total Value |

$ __________________ |

E. Insurance - Insurance on decedent's life (owned by the decedent).

Total Value $ __________________

Under penalty of perjury, I declare that I have examined this report, including any accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete.

Personal Representative / Surviving Joint Tenant / Attorney

Name (typed or printed) |

|

Social security number or federal employer identification number |

|

|

|

Address |

|

|

|

|

|

City |

State |

ZIP code |

|

|

|

Signature of representative |

Date |

Phone number |

ADOR

File Properties

| Fact | Description |

|---|---|

| Purpose of Form 74 | This form is a Report of Personal Representative of Decedent, used to report estate assets and values to the Arizona Department of Revenue. |

| Submission Address | Completed forms should be returned to the Estate Tax Unit at the Arizona Department of Revenue, 1600 W Monroe, Room 610, Phoenix AZ 85007-2650. |

| Contact Information | For assistance, individuals can call (602) 542-4643 or (800) 352-4090 (nationwide toll free), or visit www.revenue.state.az.us. |

| Types of Waivers | Section II of the form requests information on the type of waiver(s) being requested: Estate tax waiver (Real Estate) or Estate tax with waiver (Probate). |

| Governing Law | The form is governed by Arizona state laws pertaining to estate administration and taxation. |

| Documentation Requirement | For original reports, a copy of the death certificate must be attached to the form. |

| Verification | The personal representative, surviving joint tenant, or attorney must declare under penalty of perjury that the information provided is true, correct, and complete. |

Instructions on Writing Arizona 74

Filling out the Arizona 74 form is a crucial step in managing the estate of a deceased person. This form, required by the Arizona Department of Revenue, provides a comprehensive account of the decedent's assets and helps to ensure proper handling of the estate according to state laws. For personal representatives or attorneys tasked with this responsibility, a clear understanding of how to complete this form accurately is pivotal. Before you start, ensure you have all necessary documents and figures regarding the estate's assets. Remember, accuracy and honesty are paramount when declaring assets and values. Here's a step-by-step guide to help you through the process.

- Gather all required information: Before you begin, ensure you have the decedent's death certificate, federal identification number, social security number, details about the estate's assets (real estate, bank deposits, securities, other assets, and insurance), and any probate information if applicable.

- Identify the type of report: Mark whether this is an original or amended report at the top of the form.

- Provide basic information: Fill in the estate's federal identification number, the name of the decedent, the decedent's social security number, date of death, and the residence of the decedent including city, state, and ZIP code.

- Enter Probate Court details: If applicable, include the probate number and the county where the Probate Court is located.

- List representative and attorney information: Include the name, address, and contact details for the personal representative and attorney managing the estate.

- Attach a copy of the death certificate: If this is an original report, attach a version of the death certificate as instructed.

- Complete Section III first as instructed: Start by providing detailed information about the estate's assets including real estate, bank deposits, securities, and other assets. Use additional sheets if necessary.

- Fill in the Summary of Estate in Section I: After detailing the estate's assets in Section III, summarize the values in Section I according to the categories provided.

- Indicate if a federal estate tax return is being filed: Check the appropriate box to answer YES or NO.

- Specify the documents requested in Section II: Indicate the type of waiver(s) you are requesting.

- Sign the form: The personal representative, surviving joint tenant, or attorney must sign the form, providing their name, relationship to the decedent, social security number or federal employer identification number, address, and contact number. Verify the accuracy of the information by signing under the penalty of perjury statement.

- Submit the form: Double-check the form for completeness and accuracy, then submit it to the Estate Tax Unit at the Arizona Department of Revenue's address provided on the form. Consider keeping a copy for your records.

Upon completing and submitting the Arizona 74 form, the Arizona Department of Revenue will review the information provided. This step is crucial in the estate management process, ensuring that all assets are accounted for and that the estate is in compliance with state requirements. The Department may contact you for additional information or clarification. It's advisable to respond promptly to any such inquiries to avoid delays in the estate's settlement. Efficient and accurate completion of this form helps to streamline the process, making it easier for the personal representatives or attorneys involved and ensuring peace of mind for all parties concerned.

Listed Questions and Answers

What is the purpose of the Arizona Form 74?

The Arizona Form 74, also known as the Report of Personal Representative of Decedent, is a document that must be filed with the Arizona Department of Revenue by the personal representative of an estate. Its primary purpose is to report the assets of a deceased person's estate to ensure compliance with state tax requirements. The form provides a detailed summary of the estate's assets, including real estate, bank deposits, securities, other assets like household furnishings and vehicles, and insurance monies. Filing this report helps in the determination of any estate tax obligations under Arizona law.

Who is required to file the Arizona Form 74?

This form must be completed and filed by the personal representative of the decedent's estate. A personal representative can be an executor, administrator, or anyone else in charge of the deceased person's estate, appointed under the law. If the estate is going through a probate process, the person appointed by the Probate Court usually files the form. The requirement to file applies regardless of whether the deceased was a resident or non-resident of Arizona, as long as they owned assets within the state.

What documents need to be attached with the Arizona Form 74?

If you are submitting an original report, a copy of the death certificate must be attached to the Form 74. Additionally, depending on the estate's assets, you might need to attach legal descriptions of real estate located in Arizona, including all required details such as the lot number and subdivision name. It's also recommended to attach any other documentation that supports the values reported on the form, such as bank statements, stock certificates, and insurance policies, to ensure the accuracy and completeness of the estate's asset summary.

Is there a deadline for filing the Arizona Form 74?

While the Arizona Department of Revenue does not specify a strict filing deadline for Form 74 on the document itself, it is generally expected that the form is filed in a timely manner following the death of the estate holder. To avoid any potential complications or legal implications, personal representatives should aim to file the report as soon as reasonably possible after assuming their duties. If you're unsure about the exact timing or if you anticipate delays, it's advisable to contact the Estate Tax Unit directly for guidance.

Can you file an amended Arizona Form 74?

Yes, if after filing an original report you discover inaccuracies or omissions in the information provided, you can file an amended Arizona Form 74. To do this, you must indicate on the form that it is an amended submission by checking the appropriate box at the top. Ensure that all changed or updated information is accurately reported, and attach any new or revised documents that support the amendment. Filing an amended report is important to ensure that the estate's records with the Arizona Department of Revenue are correct and up-to-date.

Common mistakes

- Not attaching a copy of the death certificate when submitting an original report. This document is crucial for providing proof of death and initiating the estate process.

- Failing to accurately report all assets, including real estate, bank deposits, securities, other personal property, and insurance. Accurate reporting in Section III and the summary in Section I provides a clear snapshot of the estate's total value.

- Omitting the lot number and subdivision name when listing real estate assets. This information, required for a complete description of any real estate in Arizona, can be found on the deed to the property or the notice of valuation from the county assessor’s office.

- Incorrectly calculating the total value of the estate by not properly adding the values entered in Sections I and III. This miscalculation can result in inaccuracies in estate valuation, potentially affecting tax calculations.

- Forgetting to indicate whether a federal estate tax return (Form 706 or 706NA) is being filed. This question, found in Section I, is essential for the Arizona Department of Revenue to understand the estate's tax obligations.

- Not using a continuation sheet when more space is needed, especially when listing real estate, bank deposits, securities, and other assets. This omission can lead to incomplete asset reporting and potential oversight in estate valuation.

In addition to these common mistakes, it's also critical to properly identify the type of waiver(s) being requested in Section II, ensuring that all requests for estate tax waivers, whether for real estate or probate, are clearly indicated. Attention to detail in completing the Arizona Form 74 can prevent delays and ensure accurate handling of the decedent's estate.

Documents used along the form

When dealing with the aftermath of a loved one's death, the Arizona Form 74, also known as the Report of Personal Representative of Decedent, is just the beginning. This form helps the Arizona Department of Revenue get a clearer picture of the estate left behind. However, to comprehensively address all responsibilities and legal requirements, several other documents commonly accompany this form during the estate settlement process. Each serves a unique purpose in ensuring the estate is managed and distributed according to state laws and the decedent’s wishes.

- Death Certificate: A certified copy of the death certificate is essential for legal transactions following a death. It proves the death and details the date and place of occurrence. This document is required for transferring ownership of assets, claiming life insurance proceeds, and many other steps in settling an estate.

- Last Will and Testament: This document outlines the decedent’s wishes regarding the distribution of their estate. It typically names an executor or personal representative to manage the estate’s affairs. Validating this document in probate court is often the first step in the legal process.

- Letters of Testamentary or Letters of Administration: Issued by the probate court, these letters grant the executor or personal representative the authority to act on behalf of the decedent’s estate. They are necessary to access financial accounts, manage assets, and carry out other duties.

- Notice to Creditors: This notice is published in a local newspaper and may be sent directly to known creditors. It informs creditors of the decedent’s death and invites them to file claims against the estate for debts owed.

- Inventory of Assets: An itemized list of all assets within the estate, including real estate, personal property, bank accounts, and securities. The inventory provides a clear view of the estate’s value and helps ensure fair distribution among heirs and beneficiaries.

- Appraisal Reports: Professional appraisals may be needed to determine the fair market value of certain estate assets such as real estate, antiques, and unique personal property. These reports are crucial for accurate estate valuation and tax calculations.

- Estate Tax Returns (Federal and State): If the estate exceeds certain thresholds, estate tax returns must be filed with the IRS and potentially the state’s department of revenue. These returns calculate the estate’s tax liability based on its value and applicable tax laws.

Together, these documents form a comprehensive package that addresses the detailed requirements of estate settlement. They work in conjunction with Arizona Form 74 to ensure that personal representatives can fulfill their duties accurately and legally, alleviating some of the burdens that come with managing the final affairs of a loved one.

Similar forms

The Form 706, or the United States Estate (and Generation-Skipping Transfer) Tax Return, shares similarities with Arizona Form 74 in that it is used to report the assets of a decedent. Both forms require a comprehensive listing and valuation of estate assets, including real estate, bank deposits, securities, and other personal property. Additionally, they inquire about life insurance owned by the decedent. Where Form 706 is used for federal tax purposes to determine any owed estate tax, Arizona's Form 74 is used specifically within the state for similar reporting purposes, often in absence of or alongside the federal requirement.

The Form 706-NA, or the United States Estate (and Generation-Skipping Transfer) Tax Return for Nonresident Aliens, parallels Arizona Form 74 by catering to a specific group—nonresident aliens, as opposed to residents or citizens of the United States. Both forms demand detailed asset listings within their respective jurisdictions. While Form 706-NA focuses on the U.S. assets of a deceased nonresident alien, Form 74 targets all the assets located within Arizona or owned by its residents at the time of death, illustrating the geographical focus both forms have, albeit at different jurisdictional levels.

The Inventory and Appraisement form, commonly used in probate proceedings, closely aligns with Arizona Form 74 by listing assets belonging to a decedent's estate. Both serve as tools for gathering comprehensive asset details post-death, such as real estate, personal property, and financial accounts. These forms are pivotal in evaluating the estate’s total worth, facilitating a smoother process in probate court by offering a clear asset overview to all parties involved, including the court itself, beneficiaries, and any debt collectors.

The Affidavit for Collection of Personal Property, another probate-related document, shares its purpose with Arizona Form 74 in that it allows for the transfer of assets without formal probate proceedings for smaller estates. While the Affidavit simplifies asset transfer based on a sworn statement for estates below a certain threshold, Form 74 provides a detailed accounting of the decedent's assets to the Arizona Department of Revenue, which can include information relevant for smaller estate assessments or waivers.

Transfer on Death (TOD) Registration forms for securities parallel the Arizona Form 74 in documenting the decedent’s securities at the time of death. Both forms contribute to transferring ownership of assets like stocks and bonds, with TOD forms directly registering beneficiaries for these assets, circumventing probate. In contrast, Form 74 lists these assets as part of the estate valuation, potentially subject to estate tax considerations within Arizona.

The Death Certificate is inherently linked to the Arizona Form 74, as it serves as a foundational document that must accompany the Form 74 if it's an original report. The death certificate provides official proof of death and is crucial for processing the estate, including the validation and execution of Form 74’s asset report. Both documents together help to solidify the estate's status and facilitate the appropriate administrative and tax-related proceedings.

Life Insurance Forms that claim benefits due to a policyholder's death resemble the purpose of Arizona Form 74 by recognizing and quantifying assets attributable to the decedent, specifically through life insurance proceeds. While life insurance forms aim to direct these proceeds to the named beneficiaries, Form 74 includes these amounts in the estate’s total valuation if owned by the decedent, impacting the estate’s overall financial assessment and subsequent tax or waiver applications.

Real Estate Deeds are closely related to the information required on Arizona Form 74, as both document ownership and value of real property. When completing Form 74, legal descriptions and values of real estate owned by the decedent in Arizona must be listed, similar to how real estate deeds establish and record property ownership. These details are crucial for assessing the estate's total real estate holdings and for any real estate transfers that may occur through probate proceedings.

The Will or Last Testament, while primarily a directive document, overlaps with Arizona Form 74 in providing a record of the decedent's intentions for asset distribution. While a will outlines how and to whom assets should be distributed, Form 74 compiles a list of these same assets for tax reporting purposes. Both documents work in tandem during probate to ensure the decedent’s property is accounted for and distributed according to their wishes and state laws.

Bank Statement and Account Registrations serve a function similar to part of the Arizona Form 74 by detailing financial accounts, including the type of account and balance at the time of death. These financial documents are essential for completing the Form 74 accurately, providing a snapshot of the decedent’s liquid assets. These values are integral to calculating the estate's total worth, affecting any tax liabilities or waivers the estate may be eligible for within Arizona.

Dos and Don'ts

Filling out the Arizona Form 74, which is the Report of Personal Representative of Decedent, requires attention to detail and accuracy. Below are the fundamental do's and don'ts to ensure the process is conducted smoothly and correctly.

Do's:

Complete Section III first, as advised in the instructions of the form. It’s designed to help you summarize the estate effectively in Section I.

Ensure all fields are printed in a legible manner to prevent misunderstandings or processing delays. If typing is not an option, use clear and readable handwriting.

Attach a copy of the decedent’s death certificate if you are submitting an original report. This document is crucial for verifying the information provided.

Include accurate valuations for all estate assets, such as real estate, bank deposits, and other pertinent property types listed in Section III. These figures are vital for a correct assessment of the estate value.

Sign the form and declare, under penalty of perjury, that the information provided is true, correct, and complete to the best of your knowledge and belief.

Don'ts:

Don’t leave any sections incomplete, especially if they apply to the estate. Every piece of information requested plays a vital role in the report’s accuracy.

Avoid guessing values of assets. If unsure, consult a valuation expert or seek assistance from the Arizona Department of Revenue to get as accurate a figure as possible.

Do not submit the form without reviewing all the information for completeness and accuracy. Double-check entries, especially numbers and financial figures.

Resist the urge to submit the report without the required attachments, such as the death certificate for original reports or additional documentation for asset verification.

Don’t forget to list all assets, including household furnishings, motor vehicles, and any insurance on the decedent’s life that they owned. Omitting assets can lead to an incomplete report.

By following these guidelines, you can help ensure that the Report of Personal Representative of Decedent (Form 74) is filled out comprehensively and accurately, thereby avoiding potential delays or issues in the estate’s processing.

Misconceptions

Understanding the Arizona Form 74, the Report of Personal Representative of Decedent, can sometimes be confusing. Here are some common misconceptions about the form:

- All assets need to be listed in detail. While it's true that the form requires a comprehensive listing of the decedent's assets, it's structured to group assets into categories (like real estate, bank deposits, etc.) rather than requiring an item-by-item inventory. Values are reported in aggregate per category.

- The form is only for Arizona residents. This misconception arises because the form focuses on assets located in Arizona. However, it must be completed for any decedent who owned real estate or other taxable property in Arizona, regardless of their state of residence at the time of death.

- Filing the Arizona 74 form means taxes are owed. The main objective of the form is to report the assets of the decedent for state tax evaluation purposes. Whether estate taxes are actually owed depends on the value of the estate and other factors. Filing the form does not automatically imply that estate taxes are due.

- Personal representatives can skip Section III if they're unsure about asset values. Section III, detailing estate assets, is a critical part of the form. If exact values are unknown, estimates should be used, and adjustments can be made later. Skipping this section is not advised as it can result in incomplete filing and potential penalties.

- Attaching a death certificate is optional. If this is the original report being filed, attaching a copy of the death certificate is a required step. This document is essential for the processing of the form and verifying the decedent's information.

- The form is only for use by personal representatives. While the form is termed "Report of Personal Representative of Decedent," it may also be completed by surviving joint tenants or attorneys representing the estate, not exclusively by personal representatives. The appropriate party should declare their capacity when signing the document.

Overall, completing the Arizona 74 form is a necessary step in managing a decedent's estate in Arizona. Careful attention to instructions and thoroughness in reporting can ease the process and ensure compliance with Arizona's Department of Revenue requirements.

Key takeaways

Filling out and using the Arizona Form 74, known as the Report of Personal Representative of Decedent, is an important step in managing the estate of a deceased person in Arizona. Here are eight key takeaways to guide individuals through this process:

- The form should be returned to the Estate Tax Unit of the Arizona Department of Revenue, evidence of the state's intention to oversee the proper distribution and taxation of an estate.

- It is crucial to indicate whether the form being filed is the original report or an amended one, signifying the fluid nature of estate management where initial reports may require updates.

- The requirement for the estate's federal identification number, the decedent's social security number, and the date of death emphasizes the importance of proper identification and confirms the financial and legal implications of death.

- Attaching a copy of the death certificate for original reports underscores the necessity of official documentation in validating the death and the commencement of estate proceedings.

- Completing Section III before the summary segment (Section I) is advised, highlighting the need for a detailed account of assets to inform the summary accurately.

- Specifying assets located both in Arizona and elsewhere allows for clarity in asset distribution and tax obligations, ensuring compliance with both state and federal laws.

- The inquiry about filing a federal estate tax return points to the interconnectedness between state and federal tax obligations following a death.

- The declaration under penalty of perjury by the personal representative, surviving joint tenant, or attorney solidifies the document's legal standing, emphasizing the seriousness and legal implications of the information provided.

Understanding these key aspects ensures that the process is handled accurately and efficiently, honoring the decedent's estate and meeting legal requirements.

Discover Common PDFs

Arizona Filing Requirements - Streamlines the divorce filing process for individuals in Yavapai County by providing specific sections for disclosing marital and financial details.

Arizona Income Tax Forms - Guides applicants through selecting the appropriate license type, including special categories like TPT for cities only.