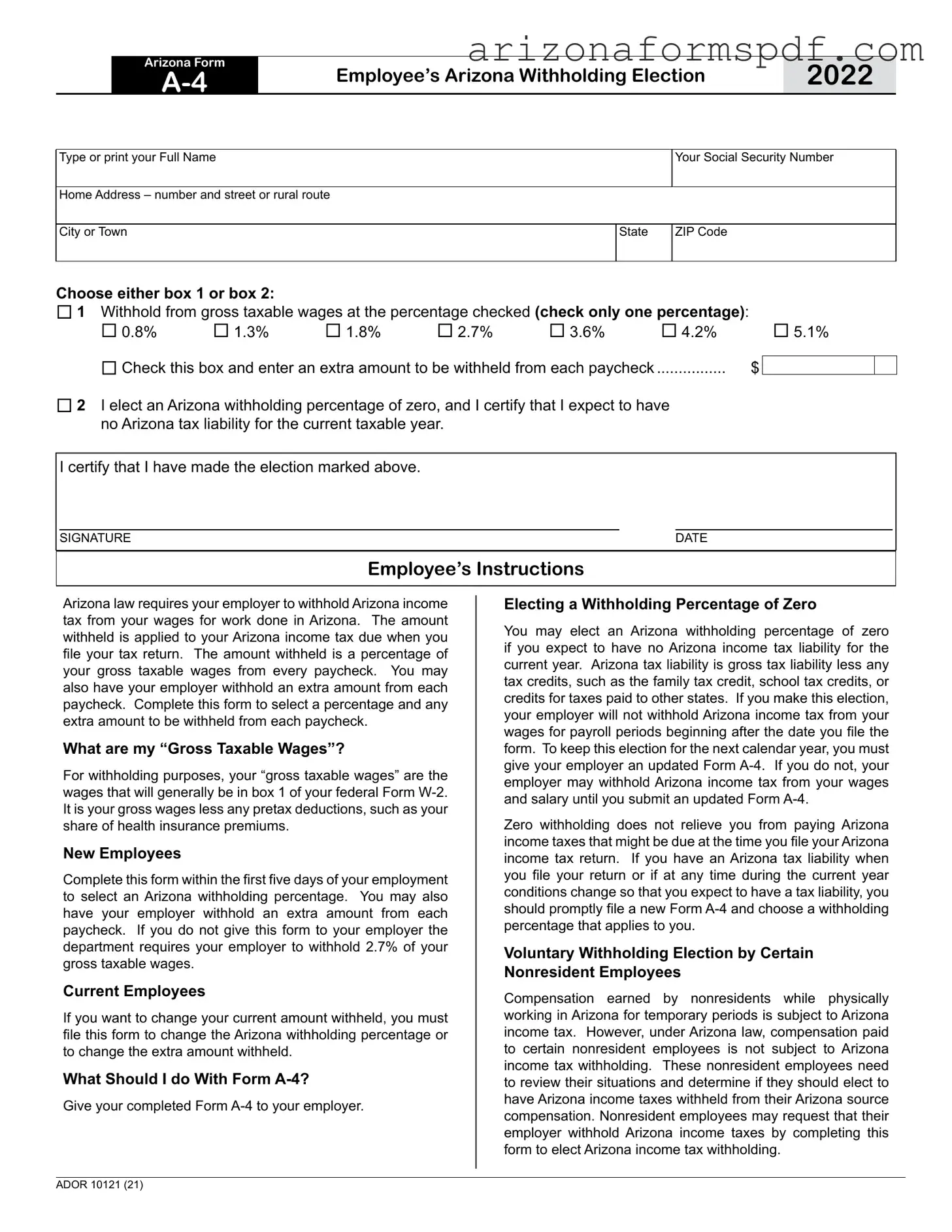

Fill in Your Arizona A4 Form

Understanding the Arizona Form A-4, also known as the Employee’s Arizona Withholding Election, is crucial for both employers and employees. This pivotal document guides the process of withholding state income tax from employees' wages in Arizona. Filling out this form accurately can impact one’s financial situation, ensuring that the right amount of tax is withheld throughout the year to meet Arizona income tax liabilities. The form provides options for selecting a withholding percentage or electing zero withholding if the employee expects to have no Arizona tax liability for the year. Additionally, it allows for specifying an extra amount to be withheld from each paycheck, offering individuals further control over their withholdings. It is essential for new employees to complete this form within the first five days of employment, whereas current employees must submit this form to adjust their withholding rates or extra withholding amounts. The choice of withholding percentage is critical, with options ranging from 0.8% to 5.1%, catering to different financial situations and anticipated tax liabilities. Moreover, special provisions are in place for nonresident employees working temporarily within the state, highlighting the form’s comprehensive approach to accommodative taxpayer needs. Furthermore, zero withholding can be a significant election for those expecting no tax liability, although it does not exempt one from filing a tax return or paying due taxes. Therefore, understanding and correctly completing the Arizona A-4 form is imperative for managing one’s income tax withholding effectively, ensuring compliance with state tax requirements while optimizing one’s financial planning.

Document Preview

Arizona Form

Employee’s Arizona Withholding Election

2022

Type or print your Full Name |

|

Your Social Security Number |

|

|

|

Home Address – number and street or rural route |

|

|

|

|

|

City or Town |

State |

ZIP Code |

|

|

|

Choose either box 1 or box 2:

1 Withhold from gross taxable wages at the percentage checked (check only one percentage):

0.8% |

1.3% |

1.8% |

2.7% |

3.6% |

4.2% |

|

5.1% |

|

Check this box and enter an extra amount to be withheld from each paycheck |

|

$ |

|

|

||||

................ |

|

|

||||||

2 I elect an Arizona withholding percentage of zero, and I certify that I expect to have no Arizona tax liability for the current taxable year.

I certify that I have made the election marked above.

SIGNATURE |

DATE |

Employee’s Instructions

Arizona law requires your employer to withhold Arizona income tax from your wages for work done in Arizona. The amount withheld is applied to your Arizona income tax due when you file your tax return. The amount withheld is a percentage of your gross taxable wages from every paycheck. You may also have your employer withhold an extra amount from each paycheck. Complete this form to select a percentage and any extra amount to be withheld from each paycheck.

What are my “Gross Taxable Wages”?

For withholding purposes, your “gross taxable wages” are the wages that will generally be in box 1 of your federal Form

New Employees

Complete this form within the first five days of your employment to select an Arizona withholding percentage. You may also have your employer withhold an extra amount from each paycheck. If you do not give this form to your employer the department requires your employer to withhold 2.7% of your gross taxable wages.

Current Employees

If you want to change your current amount withheld, you must file this form to change the Arizona withholding percentage or to change the extra amount withheld.

What Should I do With Form

Give your completed Form

Electing a Withholding Percentage of Zero

You may elect an Arizona withholding percentage of zero if you expect to have no Arizona income tax liability for the current year. Arizona tax liability is gross tax liability less any tax credits, such as the family tax credit, school tax credits, or credits for taxes paid to other states. If you make this election, your employer will not withhold Arizona income tax from your wages for payroll periods beginning after the date you file the form. To keep this election for the next calendar year, you must give your employer an updated Form

Zero withholding does not relieve you from paying Arizona income taxes that might be due at the time you file your Arizona income tax return. If you have an Arizona tax liability when you file your return or if at any time during the current year conditions change so that you expect to have a tax liability, you should promptly file a new Form

Voluntary Withholding Election by Certain Nonresident Employees

Compensation earned by nonresidents while physically working in Arizona for temporary periods is subject to Arizona income tax. However, under Arizona law, compensation paid to certain nonresident employees is not subject to Arizona income tax withholding. These nonresident employees need to review their situations and determine if they should elect to have Arizona income taxes withheld from their Arizona source compensation. Nonresident employees may request that their employer withhold Arizona income taxes by completing this form to elect Arizona income tax withholding.

ADOR 10121 (21)

File Properties

| Fact Number | Fact Detail |

|---|---|

| 1 | Arizona Form A-4 is specifically designed for employees to select their withholding percentage for Arizona income tax. |

| 2 | Employees can choose to have a specific percentage of their gross taxable wages withheld, with options ranging from 0.8% to 5.1%, or elect to withhold an additional flat amount. |

| 3 | New employees must complete the Arizona Form A-4 within the first five days of employment to select their withholding percentage. |

| 4 | For employees who do not submit this form to their employer, Arizona requires the employer to withhold 2.7% of the employees' gross taxable wages. |

| 5 | Current employees wishing to change their withholding amount need to file a new Arizona Form A-4 to adjust their elected withholding percentage or the extra amount withheld. |

| 6 | Employees can elect a 0% withholding if they anticipate no Arizona tax liability for the current year, but this doesn't exempt them from potential Arizona income taxes due upon filing their return. |

| 7 | Governing law for Arizona Form A-4 is Arizona state law regarding income tax withholding for employees. |

| 8 | Nonresident employees working temporarily in Arizona can elect to have Arizona income tax withheld by completing the Arizona Form A-4. |

| 9 | This withholding election form should be completed with an employee's full name, social security number, and address, and submitted to their employer. |

Instructions on Writing Arizona A4

Filling out the Arizona A-4 form is an important step for any employee working in Arizona as it determines how much state income tax will be withheld from your paycheck. This action not only impacts your take-home pay but also influences your annual state tax filings. By selecting a withholding rate that best matches your expected tax liability, you can avoid owing a significant amount at the end of the tax year or receiving a large refund. If you're starting a new job or wish to adjust your current withholding, here are the steps to complete the Arizona A-4 form accurately.

- Begin by typing or printing your full name at the top of the form.

- Enter your Social Security Number.

- Provide your complete home address, including the number and street or rural route, city or town, state, and ZIP code.

- Decide if you want to elect a specific withholding percentage from your gross taxable wages. If so, choose either box 1 or box 2.

- If you chose box 1, select only one of the indicated percentages (0.8%, 1.3%, 1.8%, 2.7%, 3.6%, 4.2%, or 5.1%) that corresponds to the amount to be withheld from your gross taxable wages. Check the box next to your selected percentage.

- If you wish to have an additional amount withheld from each paycheck, enter that amount in the space provided under box 1.

- If you believe that you will have no Arizona tax liability for the current taxable year, check box 2 to elect an Arizona withholding percentage of zero. This choice means your employer will not withhold Arizona income tax from your wages.

- Sign and date the form to certify that the election you've made is accurate.

- Hand your completed Form A-4 to your employer.

Remember, choosing a withholding percentage of zero does not exempt you from possible Arizona income taxes due at the end of the tax year. If your financial situation changes and you anticipate owing taxes, it's crucial to update your Form A-4 with your employer to adjust your withholding. This proactive step helps ensure that the right amount is being withheld to meet your tax obligations.

Listed Questions and Answers

What is the Arizona A4 Form?

The Arizona A4 form, officially known as the Employee’s Arizona Withholding Election, is a document that employees use to determine how much state income tax their employer should withhold from their wages. It allows employees in Arizona to choose a specific percentage of gross taxable wages that will be deducted from each paycheck for state taxes. Additionally, employees can choose to have an additional amount withheld or elect a zero withholding percentage if they expect to have no Arizona tax liability for the year.

How do I complete the Arizona A4 Form?

To complete the Arizona A4 form, an employee needs to type or print their full name, Social Security Number, and address. They then choose one of the two boxes indicating their withholding preference: a specific percentage rate ranging from 0.8% to 5.1%, an additional amount to be withheld, or elect to have no Arizona income tax withheld. Once the selection is made, the form must be signed and dated. This completed form should then be given to the employer.

Who needs to fill out an Arizona A4 Form?

New employees should fill out the form within the first five days of employment to set their Arizona state tax withholding preference. Current employees who wish to change their withholding percentages or additional amount withheld also need to complete a new Form A-4 to reflect these changes.

Can I elect not to have any Arizona income tax withheld?

Yes, you can elect a withholding percentage of zero by choosing box 2 on the Arizona A4 form. This election is for employees who expect to have no Arizona income tax liability for the current year. However, if conditions change and you anticipate having a tax liability, you must submit a new Form A-4 with an appropriate withholding percentage selected to avoid tax due at the time of filing your Arizona income tax return.

What happens if I don’t submit an Arizona A4 Form?

If you do not submit a completed Arizona A4 form to your employer, the state requires your employer to withhold state income tax at a flat 2.7% from your gross taxable wages.

How do nonresident employees handle Arizona income tax withholding?

Nonresident employees working in Arizona for temporary periods are still subject to Arizona income tax withholding. However, certain nonresidents may not be required to have taxes withheld but can opt for voluntary withholding by completing the A4 form and electing their desired withholding percentage.

What are “Gross Taxable Wages”?

For the purpose of the Arizona A4 form, “gross taxable wages” refer to the wages that are subject to federal withholding for income tax purposes, generally reflected in box 1 of your federal Form W-2. This amount is your gross wages minus any pretax deductions such as health insurance premiums.

Common mistakes

Filling out the Arizona A4 form correctly is crucial for employees to ensure the accurate amount of state income tax is withheld from their wages. However, individuals often make several common mistakes when completing this form. Identifying and avoiding these errors can streamline the process, ensuring compliance with Arizona tax laws and potentially avoiding unexpected tax liabilities. Here are five common mistakes:

Incorrect Withholding Percentage: One of the most common mistakes is selecting the wrong withholding percentage. Employees either check more than one percentage box or choose a percentage that does not accurately reflect their estimated tax liability. This error can lead to either underpaying or overpaying state taxes.

Failing to Update the Form: Current employees often overlook the need to update their Arizona A4 form when their financial situation changes. Life events such as marriage, divorce, or the birth of a child can affect tax liabilities, making it crucial to adjust withholding rates accordingly.

Neglecting Optional Extra Amount: The option to have an extra amount withheld from each paycheck is frequently ignored. For individuals who anticipate owing taxes or who have specific financial goals, such as covering estimated tax due on other sources of income, this feature can be beneficial.

Misunderstanding Zero Withholding Option: Electing a zero withholding percentage without fully understanding the qualifications leads to errors. This option should only be chosen if the employee expects to have no Arizona tax liability for the year. Without proper consideration, this might result in unforeseen tax bills at year-end.

Incorrect or Incomplete Personal Information: Even simple mistakes like entering an incorrect Social Security Number or failing to provide a complete home address can delay processing. Such errors can also result in the employer withholding at the default rate rather than the employee’s chosen rate.

By steering clear of these mistakes, employees can ensure their Arizona A4 forms are accurately completed, reflecting their intended tax withholding preferences. This not only aids in managing their annual tax liabilities but also prevents potential issues with the Arizona Department of Revenue. It is always advisable for employees to review their tax situation periodically and consult with a tax professional if they are unsure how to proceed.

Documents used along the form

Understanding the importance of accurate and comprehensive documentation in employment and tax matters is crucial for both employees and employers. The Arizona A4 form is a key document for employees working in Arizona, allowing them to select their preferred withholding percentage. However, this form is just one part of a complex puzzle involving various forms and documents that ensure compliance with federal and state regulations, and facilitate smoother financial and administrative processes. Below is an overview of nine additional forms and documents often used alongside the Arizona A4 form, each serving its own unique purpose.

- Form W-4 (Employee's Withholding Certificate): Federal counterpart to the Arizona A4, instructing employers on the amount of federal income tax to withhold from an employee's wages.

- Arizona Form A-4V (Voluntary Withholding Request): Used by individuals receiving unemployment compensation to request withholding of state income tax from their benefits.

- Form W-2 (Wage and Tax Statement): Annual report provided by employers to employees and the IRS, detailing the employee's annual wages and the amount of taxes withheld.

- Form I-9 (Employment Eligibility Verification): Required by the Department of Homeland Security, this form is used by employers to verify an employee's identity and eligibility to work in the United States.

- Form 1099-MISC (Miscellaneous Income): Reports income from sources other than wages, salaries, and tips. This form is especially relevant for freelancers and contractors.

- Form 941 (Employer’s Quarterly Federal Tax Return): Used by employers to report income taxes, social security tax, or Medicare tax withheld from employees' paychecks.

- Arizona Form A-4P (Withholding Certificate for Pension or Annuity Payments): Allows individuals receiving payments from pensions or annuities to specify their Arizona state income tax withholding preferences.

- Form SS-4 (Application for Employer Identification Number): Used by businesses to apply for an employer identification number (EIN), which is necessary for tax filing and reporting purposes.

- Direct Deposit Authorization Forms: Employers may require this form to set up direct deposit of employees’ wages into their bank accounts, streamlining the payment process.

Each of these documents plays a vital role in the tapestry of employment and tax administration, helping to ensure that employees are correctly identified, compensated, and taxed. For employees, understanding the purpose and requirements of these documents can empower them to manage their employment and tax situations more effectively. For employers, meticulous attention to these documents can facilitate compliance with legal obligations, contribute to operational efficiency, and establish a foundation for a transparent and accountable employment practice.

Similar forms

The Arizona A4 form, titled "Employee’s Arizona Withholding Election," is closely related to the Federal W-4 form, "Employee's Withholding Certificate." Both forms serve the primary function of informing employers about the amount of tax to withhold from an employee's paycheck. The A4 form is specific to Arizona state tax, while the W-4 pertains to federal income tax. Employees fill out both forms to declare their withholding status, exemptions, and, if necessary, an additional amount they wish to have withheld from each paycheck. The specificity towards federal versus state tax responsibilities is the primary distinction between these two forms.

Another document akin to the Arizona A4 form is the California DE 4 form, "Employee's Withholding Allowance Certificate." Similar to the A4, the DE 4 is used by employees in California to determine state income tax withholdings. Employees use it to indicate their marital status, the number of allowances claimed, and any additional amount to be deducted. While both forms aim to customize the withholding process to better reflect the individual tax liabilities at the state level, they are tailored to the respective state tax codes and rates of Arizona and California.

The New York IT-2104 form, "Employee's Withholding Allowance Certificate," also shares similarities with Arizona's A4 form. It is designed for New Yorkers to specify their withholding preferences for state income tax. The IT-2104, like the A4, allows New York employees to choose their withholding rate based on allowances, marital status, and other income considerations. These forms both ensure that the amount of state income tax withheld from the employee's paycheck is aligned with their expected yearly tax liability, reflecting the adaptations made to accommodate state-specific tax structures.

The Form W-9, "Request for Taxpayer Identification Number and Certification," although primarily used for different purposes, shares a connectivity with the A4 in its role in the tax reporting and withholding process. The W-9 is often utilized by freelancers, independent contractors, and vendors to provide their taxpayer identification number to entities that will pay them. It ensures the correct reporting of income to the IRS. Both the W-9 and the A4 are pivotal in ensuring accurate tax documentation and withholding, even though the A4 is more focused on employment income and the W-9 caters to non-employee compensation.

Another document that parallels the Arizona A4 form is the W-2 form, "Wage and Tax Statement." The W-2 is issued by employers annually to report an employee's annual wages and taxes withheld to the IRS. While the A4 form is filled out by the employee to instruct the employer on how much to withhold, the information on the W-2 reflects the outcome of those instructions over the taxable year. Both documents are integral to the taxation process, ensuring employees' tax liabilities are met according to their reported earnings and chosen withholdings.

The 1099-MISC form, used to report various types of income outside regular wages, such as freelancer or contractor payments, shares a tangential relationship with the A4 form. While the 1099-MISC is for miscellaneous income and the responsibility of tax payments falls more directly on the recipient, the A4 deals with withholdings from a traditional employee's wages. Both documents, however, are vital for accurate income reporting and tax compliance, catering to different sources of income.

The IRS Form 1040, "U.S. Individual Income Tax Return," is another document related to the Arizona A4 form in the broader context of tax reporting and payment. The A4 form's selections influence the amount of state tax withheld, ultimately affecting the tax calculations filed on the Form 1040 for federal taxes. Essentially, while the A4 form pertains to planning and estimating state tax withholdings, the 1040 encompasses the broader scope of summarizing the individual’s total annual income, deductions, and credits to calculate federal tax liability.

The Oklahoma W-4P form, "Withholding Certificate for Pension or Annuity Payments," is an example of a specialized withholding form similar to the Arizona A4, but for pension or annuity payments rather than wages. Like the A4, it allows recipients to manage their tax withholdi.ng levels, focusing on that particular income source. Both forms empower taxpayers to tailor withholding rates to their anticipated tax obligations, although they cater to different types of income.

Georgia's G-4 form, "Employee's Withholding Allowance Certificate," serves a similar purpose as the Arizona A4 form, allowing employees to specify their withholding preferences for state income taxes. The process includes designation of allowances and additional withholding amounts, directly aligning with the A4's objectives. Despite being state-specific, both forms share the core function of personalizing the tax withholding process to better match the employee’s financial and tax situation.

Lastly, the IRS Form 8822, "Change of Address," while not directly related to tax withholding, connects to the A4 form through the importance of accurate and current information in the tax system. Form 8822 is used to notify the IRS of a change in address, ensuring that tax documents and communications are correctly directed. Similarly, updating the A4 form when personal or financial circumstances change is crucial for accurate state tax withholding. Both forms underscore the need for up-to-date information to avoid complications in tax responsibilities and refunds.

Dos and Don'ts

When you're getting ready to fill out the Arizona A4 form, it's important to keep a few key things in mind to ensure the process goes smoothly. Here's a straightforward guide to help you navigate what you should and shouldn't do.

Do:

Read the entire form carefully before attempting to fill it out. This includes understanding the definitions provided, such as what constitutes your "Gross Taxable Wages" for the purposes of this form.

Choose only one withholding percentage or elect an Arizona withholding percentage of zero if you expect to have no Arizona tax liability for the current year. Ensuring this selection aligns with your expected financial situation can help avoid future headaches.

Clearly and accurately type or print your information, including your full name, social security number, and address. This ensures that your employer and the Arizona Department of Revenue can process your form correctly.

Sign and date the form before submitting it to your employer. An unsigned form may not be processed, which could result in an incorrect withholding rate.

Don't:

Check more than one withholding percentage box in the selection area. This form is designed for you to elect a single withholding rate or elect no withholding by indicating a zero percentage; choosing more than one can invalidate your election.

Leave any sections blank that apply to you, especially your choice on the withholding percentage or if you want an additional amount withheld. An incomplete form might result in the default withholding rate being applied to your wages.

Ignore the instructions provided with the form. These instructions are designed to help you complete the form correctly and are tailored to different situations – for instance, whether you are a new employee or are electing for a zero withholding percentage.

Forget to update your form if your financial or personal circumstances change. If, for example, you initially elect a zero withholding percentage but then expect to have Arizona tax liability, you should promptly file a new Form A-4 with an appropriate withholding selection.

By following these guidelines, you can fill out the Arizona A4 form confidently and accurately, making the process smoother for both you and your employer.

Misconceptions

Understanding the Arizona Form A-4, designated for an employee's Arizona withholding election, unveils various misconceptions that often cloud its real essence and function. Here are six common misunderstandings and clarifications to provide insight into its actual operation and implications.

Misconception 1: The Form A-4 is optional for employees working in Arizona. In reality, Arizona law demands that every employee working in Arizona fills out this form within the first five days of employment. This requirement ensures the appropriate amount of Arizona income tax is withheld from one's wages.

Misconception 2: Electing a zero withholding rate on Form A-4 exempts employees from paying Arizona income taxes. While electing a zero withholding percentage means your employer will not withhold state income tax from your paycheck, it does not absolve you of any tax liability. You are still responsible for paying any Arizona income taxes due when filing your tax return.

Misconception 3: Changes in the Arizona A-4 form cannot be made after the initial submission. Employees have the flexibility to submit a new Form A-4 anytime throughout the year if they wish to adjust their Arizona withholding amount or percentage. This is especially helpful if their financial situation or expectations regarding tax liability change.

Misconception 4: If you do not submit Form A-4, no income tax will be withheld. The Arizona Department of Revenue requires employers to withhold state income tax at a default rate of 2.7% of gross taxable wages if the employee fails to submit this form.

Misconception 5: Only Arizona residents need to fill out the Arizona A-4 Form. Nonresident employees working in Arizona, especially those working temporarily, are subject to Arizona income tax on their wages earned in the state. These individuals should complete the form if they wish to have Arizona income taxes withheld, especially considering certain nonresident employees might be exempt from withholding but can still elect to have it done.

Misconception 6: Gross taxable wages are the entirety of one's paycheck. For the purposes of the Arizona A-4, "gross taxable wages" refer to your earnings that will generally appear in box 1 of your federal Form W-2, accounting for wages after certain pre-tax deductions, like health insurance premiums, have been made. This definition is crucial for accurately determining the amount subjected to the withholding tax.

Correct understanding and application of Arizona's withholding tax requirements not only facilitate compliance with state law but also ensure that employees are not met with unexpected tax liabilities come filing season. Engaging actively with the Arizona A-4 form's provisions helps employees maintain control over their financial planning and tax responsibilities.

Key takeaways

Understanding the Arizona Form A-4 and how it applies to withholding elections can guide employees through the process of accurately managing their state income tax withholdings. Here are key takeaways to note:

- The Form A-4 allows employees to select their preferred rate of income tax withholding from their wages. Options range from as low as 0.8% to as high as 5.1%.

- An option is provided for employees to have an additional amount withheld from each paycheck, offering greater flexibility in managing their tax obligations.

- Employees who anticipate no Arizona tax liability for the year can opt for a 0% withholding rate, but they must certify that they expect to have no state tax liability.

- New employees are required to complete this form within five days of starting their employment to specify their withholding percentage or to opt for additional withholding amounts.

- If a new employee does not submit this form, the employer is mandated by law to withhold at a default rate of 2.7% of the gross taxable wages.

- Current employees wishing to adjust their Arizona income tax withholding amounts must submit a new Form A-4 to either change their withholding percentage or modify the extra amount to be withheld.

- To maintain a 0% withholding election into the next calendar year, employees must submit an updated Form A-4 to their employer. Without this, the employer may begin withholding taxes again.

- Nonresident employees working in Arizona might not be subject to automatic state tax withholding but can elect to have taxes withheld by completing Form A-4. This ensures they can manage their Arizona income tax obligations proactively.

By selecting a withholding rate or extra withholding amount that aligns with their expected tax liability, employees can avoid underpayment penalties and manage their financial planning more effectively. Form A-4 provides the mechanism for making these selections and adjustments as needed, ensuring that employees can maintain control over their income tax withholdings in Arizona.

Discover Common PDFs

Arizona Tax Forms - This form is used to calculate and pay the appropriate license fees for transient selling in Arizona.

Arizona Repo Affidavit - Delivers a legal outline for Arizona lienholders on how to properly repossess and, if applicable, sell a vehicle, with particular attention to odometer disclosure.