Fill in Your Arizona Lsu Form

Understanding the nuances of the Arizona Loan Status Update (LSU) form is paramount for both buyers and sellers engaged in real estate transactions within the state. Updated in February 2013, this document plays a crucial role in the process, ensuring transparency and communication between all parties involved, including lenders and realtors. The form requires that a buyer, within five days of contract acceptance, provides a detailed account of the proposed loan's current status. It mandates lenders to update relevant parties upon request, thus encapsulating vital information ranging from pre-qualification details, loan types, and the buyer's financial dependencies, to the anticipated closing documents and dates. Critical to both the preliminary and concluding phases of the buying process, the LSU form stipulates the submission of initial and additional documentation required for loan approval, highlights the necessity of property inspections, and outlines the conditions under which a loan can be finalized. Furthermore, the form functions as a communication bridge ensuring that the seller, through the broker, is kept abreast of the financial contingencies affecting the closing process, ultimately facilitating a smoother transition towards ownership and fulfilling contractual obligations.

Document Preview

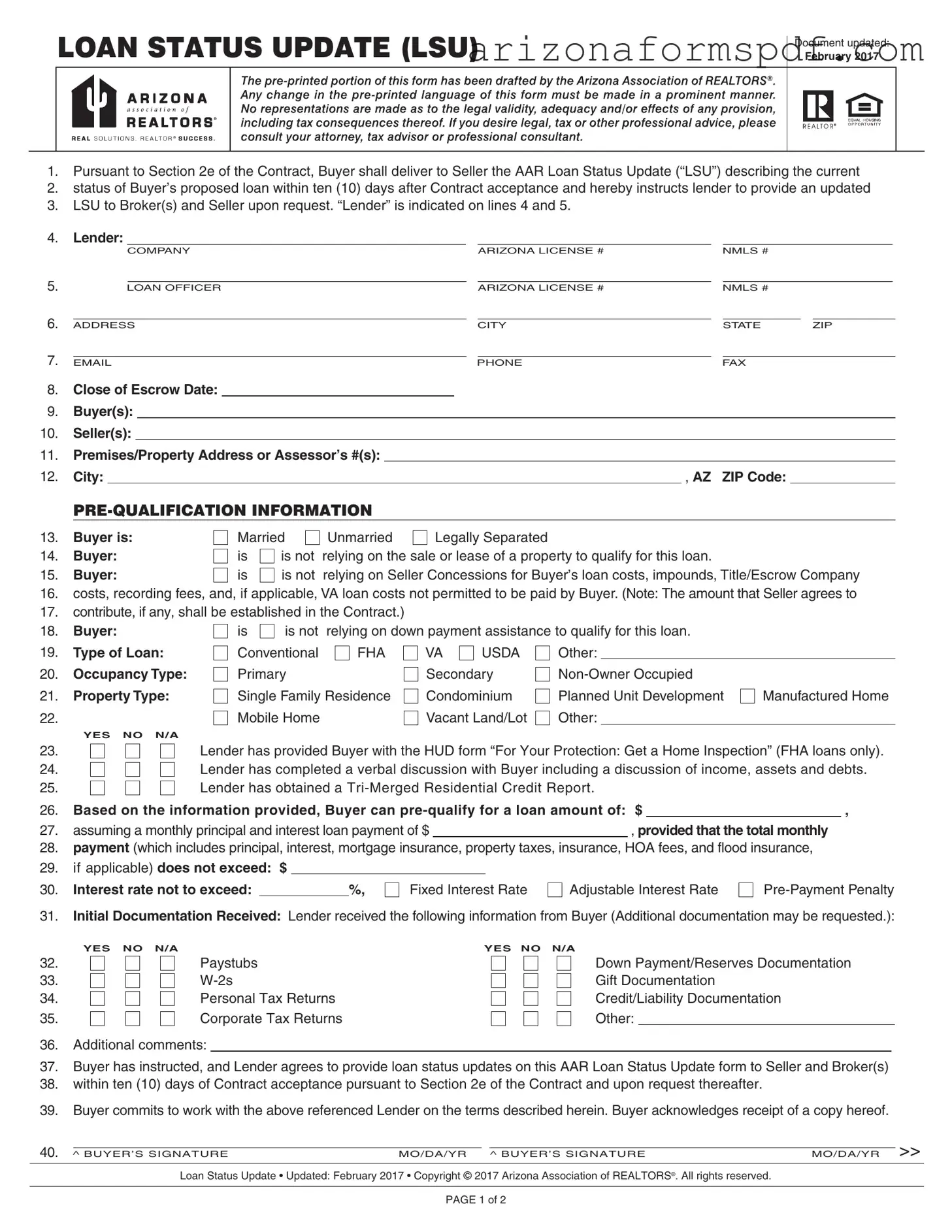

LOAN STATUS UPDATE (LSU)

Document updated:

February 2017

1.Pursuant to Section 2e of the Contract, Buyer shall deliver to Seller the AAR Loan Status Update (“LSU”) describing the current

2.status of Buyer’s proposed loan within ten (10) days after Contract acceptance and hereby instructs lender to provide an updated

3.LSU to Broker(s) and Seller upon request. “Lender” is indicated on lines 4 and 5.

4.Lender:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

COMPANY |

|

ARIZONA LICENSE # |

NMLS # |

|

|

|

||||||||

5. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

LOAN OFFICER |

|

ARIZONA LICENSE # |

NMLS # |

|

|

|

||||||||||

6. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

ADDRESS |

CITY |

|

STATE |

|

ZIP |

|

|||||||||||

7. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PHONE |

FAX |

|

|

|

|||||||||||||

8. |

Close of Escrow Date: |

|

|

|

|

|

|

|

|

|

|

|

|||||

9. |

Buyer(s): |

|

|

|

|

|

|

|

|

|

|

||||||

10. |

Seller(s): |

|

|

|

|

|

|

|

|

|

|

||||||

11. |

Premises/Property Address or Assessor’s #(s): |

|

|

|

|

|

|

|

|

|

|

||||||

12. |

City: |

|

|

|

, AZ |

ZIP Code: |

|

|

|

|

|||||||

13. |

Buyer is: |

Married |

Unmarried |

Legally Separated |

|

14. |

Buyer: |

is |

is not |

relying on the sale or lease of a property to qualify for this loan. |

|

15. |

Buyer: |

is |

is not |

relying on Seller Concessions for Buyer’s loan costs, impounds, Title/Escrow Company |

|

16.costs, recording fees, and, if applicable, VA loan costs not permitted to be paid by Buyer. (Note: The amount that Seller agrees to

17.contribute, if any, shall be established in the Contract.)

18. |

Buyer: |

is |

is not |

relying on down payment assistance to qualify for this loan. |

|

||||

19. |

Type of Loan: |

Conventional |

FHA |

VA |

USDA |

Other: |

|

|

|

20. |

Occupancy Type: |

Primary |

|

Secondary |

|

||||

21. |

Property Type: |

Single Family Residence |

Condominium |

Planned Unit Development |

Manufactured Home |

||||

22. |

|

Mobile Home |

|

Vacant Land/Lot |

Other: |

|

|

||

|

YES NO N/A |

|

|

|

|

23. |

Lender has provided Buyer with the HUD form “For Your Protection: Get a Home Inspection” (FHA loans only). |

||||

24. |

Lender has completed a verbal discussion with Buyer including a discussion of income, assets and debts. |

||||

25. |

Lender has obtained a |

|

|

|

|

26. |

Based on the information provided, Buyer can |

|

, |

||

27. |

assuming a monthly principal and interest loan payment of $ |

|

, provided that the total monthly |

|

|

28.payment (which includes principal, interest, mortgage insurance, property taxes, insurance, HOA fees, and flood insurance,

29.if applicable) does not exceed: $

30. Interest rate not to exceed: |

|

%, |

Fixed Interest Rate |

Adjustable Interest Rate |

31.Initial Documentation Received: Lender received the following information from Buyer (Additional documentation may be requested.):

YES NO N/A |

YES NO N/A |

32.

33.

34.

35.

Paystubs

Personal Tax Returns

Corporate Tax Returns

Down Payment/Reserves Documentation

Gift Documentation

Credit/Liability Documentation

Other:

36.Additional comments:

37.Buyer has instructed, and Lender agrees to provide loan status updates on this AAR Loan Status Update form to Seller and Broker(s)

38.within ten (10) days of Contract acceptance pursuant to Section 2e of the Contract and upon request thereafter.

39.Buyer commits to work with the above referenced Lender on the terms described herein. Buyer acknowledges receipt of a copy hereof.

40. |

|

|

|

|

|

>> |

^ BUYER’S SIGNATURE |

MO/DA/YR ^ BUYER’S SIGNATURE |

MO/DA/YR |

||||

|

|

|

|

|

|

|

Loan Status Update • Updated: February 2017 • Copyright © 2017 Arizona Association of REALTORS®. All rights reserved.

PAGE 1 of 2

Page 2 of 2

Loan Status Update (LSU) >>

Premises/Property Address or Assessor’s #(s):

DOCUMENTATION

|

DATE |

LENDER |

YES NO |

COMPLETED |

INITIALS |

41.

42.

43.

44.

45.

46.

47.

48.

49.

50.

51.

52.

53.

54.

55.

56.

57.

58.

Lender received the Contract and all Addenda |

/ |

/ |

||||||

Lender received Buyer’s name, income, social security number, Premises address, |

|

|

|

|

|

|

||

estimate of value of the Premises, and mortgage loan amount sought |

|

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

Lender sent Loan Estimate |

|

/ |

/ |

|||||

Buyer indicated to Lender an intent to proceed with the transaction after having |

|

|

|

|

|

|

||

received the Loan Estimate |

|

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

Lender received a signed Form 1003 and Lender disclosures |

|

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

Payment for the appraisal has been received |

|

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

Lender ordered the appraisal |

|

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

Lender identified down payment source |

|

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

Lender received and reviewed the Title Commitment |

|

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

Buyer locked the loan program and financing terms, including interest rate and points |

|

/ |

/ |

|||||

Lock expiration date |

|

|

|

|

|

|

|

|

Lender received the Initial Documentation listed on lines |

|

/ |

/ |

|||||

|

|

|

|

|

|

|||

Appraisal received |

|

/ |

/ |

|||||

|

|

|

|

|

|

|||

Premises/Property appraised for at least the purchase price |

|

/ |

/ |

|||||

|

|

|

|

|

|

|||

Closing Disclosure provided to Buyer |

|

/ |

/ |

|||||

|

|

|

|

|

|

|||

Closing Disclosure received by Buyer |

|

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

UNDERWRITING AND APPROVAL

59.

60.

61.

62.

Lender submitted the loan package to the Underwriter |

|

/ |

/ |

||

|

|

|

|

|

|

Lender obtained loan approval with Prior to Document (“PTD”) Conditions |

|

/ |

/ |

||

|

|

|

|

|

|

Appraisal conditions have been met |

|

/ |

/ |

||

|

|

|

|

|

|

Buyer has loan approval without PTD Conditions |

|

/ |

/ |

||

|

|

|

|

|

|

CLOSING

63.

64.

65.

66.

67.

68.

69.

Lender ordered the Closing Loan Documents and Instructions |

|

/ |

/ |

|||

|

|

|

|

|

|

|

Lender received signed Closing Loan Documents from all parties |

|

/ |

/ |

|||

|

|

|

|

|

|

|

All Lender Quality Control Reviews have been completed |

|

/ |

/ |

|||

All Prior to Funding (“PTF”) Conditions have been met and Buyer has obtained |

|

|

|

|

|

|

loan approval without conditions |

|

/ |

/ |

|||

|

|

|

|

|

|

|

Funds have been ordered |

|

/ |

/ |

|||

|

|

|

|

|

|

|

All funds have been received by Escrow Company |

|

/ |

/ |

|||

|

|

|

|

|

|

|

70.Close of escrow occurs when the deed has been recorded at the appropriate county recorder’s office.

71. |

|

|

^ LOAN OFFICER’S SIGNATURE |

MO/DA/YR |

Loan Status Update • Updated: February 2017 • Copyright © 2017 Arizona Association of REALTORS®. All rights reserved.

PAGE 2 of 2

File Properties

| Fact Name | Description |

|---|---|

| Document Identification | The document is known as the Loan Status Update (LSU), updated in February 2013. |

| Primary Purpose | The LSU serves to communicate the current status of the Buyer's proposed loan to the Seller. |

| Submission Timeline | It must be delivered to the Seller within five (5) days after contract acceptance. |

| Involved Parties | The LSU involves multiple parties including the Buyer, Seller, Lender, and Broker(s). |

| Governing Law | The form is governed by the Arizona Association of REALTORS® and its stipulations are made pursuant to Section 2e of the Contract outlined within the LSU. |

Instructions on Writing Arizona Lsu

After entering into a contract for purchasing a property, you will need to complete and provide the Arizona Loan Status Update (LSU) form within five days. This document communicates the current status of your proposed loan from you, the buyer, to the seller. It's also used to instruct the lender to share updates with both the broker(s) and the seller upon request. Here’s how to accurately complete the form:

- Identify the lender on lines 4 and 5 by filling in the company name and Arizona license number.

- Provide the loan officer's contact information, including NMLS number, address, email, and phone and fax numbers on lines 5 through 8.

- List the anticipated closing and loan documents delivery dates on line 8.

- Fill in the buyer(s) and seller(s) names on lines 9 and 10, ensuring accuracy for legal clarity.

- On line 11, enter the premises or property address or assessor’s number(s), along with the city, state, and ZIP code on the subsequent lines.

- Indicate the buyer’s marital status, whether relying on the sale or lease of a property to qualify for the loan, and if seller concessions are expected to cover loan costs on lines 13 through 21.

- Specify the type of loan, occupancy type, and property type by marking the appropriate boxes from lines 18 through 21.

- If applicable, confirm the lender has provided the HUD form “For Your Protection: Get a Home Inspection” on line 22 (for FHA loans only).

- Acknowledge that the lender has completed a verbal discussion about income, assets, and debts, and obtained a Tri-Merged Residential Credit Report on lines 23 and 24.

- Enter the pre-qualified loan amount and maximum monthly payment, including all specified expenses, on lines 25 through 28.

- List the initial requested documentation provided by the buyer to the lender, marking the appropriate boxes for each document type on lines 32 through 35.

- Add any additional comments regarding the loan application or approval process that might be helpful for the seller or broker(s) on line 36.

- Ensure the buyer and loan officer sign and date the form where indicated on the bottom of the pages.

Completing the Arizona Loan Status Update form with care and precision ensures that all parties involved in the property transaction are well-informed about the loan's status and any actions required moving forward. Always double-check the information for accuracy before submitting the form to avoid any unnecessary delays in the loan processing and property purchase timeline.

Listed Questions and Answers

What is the purpose of the Arizona Loan Status Update (LSU) form?

The Arizona Loan Status Update (LSU) form serves as a critical communication tool between the buyer, lender, and seller during a real estate transaction. Its main purpose is to keep all parties informed about the current status of the buyer's mortgage application process. By outlining the progress of the loan, from pre-qualification to closing, it ensures transparency and helps in maintaining the timelines outlined in the real estate contract.

When should the LSU form be submitted in the process of a real estate transaction?

According to the stipulations set out in the contract, the buyer is required to deliver the LSU to the seller within five days after the acceptance of the contract. Furthermore, the lender is instructed to provide updated LSUs to both the broker(s) and seller upon request, ensuring that all parties are kept up-to-date with the latest developments in the loan process.

Who is responsible for filling out and updating the LSU form?

The lender, as indicated on the form, bears the primary responsibility for filling out and updating the LSU. The buyer initiates this process by instructing the lender to complete and provide updates on the form as required. It's essential for the lender to provide accurate and timely updates to facilitate smooth communication between all parties involved in the transaction.

What type of information is included in the LSU form?

The LSU form encompasses a wide range of information related to the buyer's loan application. This includes pre-qualification details, the type of loan, occupancy, property type, lender's details, and specifics about the buyer’s financial situation such as income, assets, debts, and the pre-qualification loan amount. The form also tracks the progress of various stages in the loan process, from initial documentation submission to loan approval and closing activities.

What happens if there are delays or issues with the loan application as reported on the LSU?

If delays or issues arise with the loan application as reported on the LSU, it's imperative for the lender to communicate these developments promptly. This allows all parties involved to address the concerns and make necessary adjustments to the timeline or terms of the contract, if applicable. Transparency and open communication facilitated by the LSU help in mitigating any potential impacts on the closing process.

Common mistakes

Filling out the Arizona Loan Status Update (LSU) form is a crucial step in the home buying process, ensuring clear communication between buyers, sellers, and lenders regarding the financing of the purchase. However, it's common for individuals to encounter a few stumbling blocks along the way. By becoming aware of these potential mistakes, individuals can streamline their experience, ensuring a smoother transaction for all parties involved.

Not submitting the LSU within the specified timeframe: According to the form, the buyer must deliver the AAR Loan Status Update to the seller within five days after contract acceptance. Delaying this submission can cause unnecessary delays and confusion in the home-buying process.

Inaccurate lender information: Lines 4 and 5 of the form require the lender’s company name and Arizona license number, along with the loan officer's NMLS number. Providing incorrect information here can mislead sellers and brokers, potentially halting the process.

Omitting details about loan type and terms: The form asks for specifics regarding the type of loan, occupancy type, and property type. Skipping these details or filling them inaccurately can lead to misunderstandings about the buyer’s financing and the property in question.

Failing to indicate dependency on sale or lease of another property: The form requires disclosure on whether the buyer is relying on the sale or lease of another property to finance the loan. Overlooking this section can complicate the financial assessment and approval process.

Overlooking initial requested documentation: The form lists several types of documentation that may be required at the initiation of the loan process. Failing to check appropriate boxes or indicate N/A where necessary can slow down the application process, as it may appear that crucial documents are missing.

Understanding and avoiding these common mistakes can help ensure that your home purchase moves forward without unnecessary setbacks. Attention to detail and clear communication with your lender and real estate professional are key components of a successful transaction.

Documents used along the form

When engaging in the process associated with the Arizona Loan Status Update (LSU) form, several other documents and forms are usually involved to ensure a smooth transaction and compliance with legal and financial regulations. These documents serve various purposes, from providing detailed financial information to ensuring the property in question is accurately represented and legally clear for sale. Understanding each document's role can help all parties involved in real estate transactions navigate the process more effectively.

- Pre-Qualification Letter: This letter from a lender estimates how much the buyer might be able to borrow based on preliminary financial information. It's essential for proving a buyer's potential to afford the property.

- Purchase Agreement: This legally binding contract outlines the terms and conditions of the property sale, including price and closing date. It's a crucial document that formalizes the agreement between the buyer and seller.

- Title Report: The title report reveals any existing easements, liens, or other encumbrances on the property. Essential for ensuring the property can be transferred without legal issues, it helps protect both the buyer and the lender's interests.

- Appraisal Report: An appraisal report gives an estimate of the property's value. Lenders require this to ensure the property is worth the loan amount. It's a critical part of determining how much can be borrowed.

- Closing Disclosure: This document provides the final details about the mortgage loan, including the interest rate, loan fees, and other costs. It's crucial for the buyer to review before closing to ensure all financial terms are as agreed.

- Home Inspection Report: Although not always required by the lender, a home inspection report is vital for the buyer. It details the condition of the property and can highlight potential issues that may need to be addressed before closing.

Together, these documents complement the Arizona Loan Status Update form by ensuring that all aspects of the loan process are transparent and agreed upon by all parties involved. Each document contributes to a comprehensive view of the financial and physical condition of the property, as well as the terms of sale, helping to protect the interests of both the buyer and the lender throughout the transaction process.

Similar forms

The Loan Estimate form is a document that provides estimates of the loan terms, projected payments, and closing costs for a mortgage. It is notably similar to the Arizona Loan Status Update (LSU) form in that both deliver crucial information about the terms and costs associated with a mortgage. The Loan Estimate is typically provided to the borrower within three days of applying for a mortgage, mirroring the LSU's focus on timely communication. However, unlike the LSU, which updates all parties about the status of the loan process, the Loan Estimate primarily serves to inform the borrower about the expected costs at the outset of the loan application process.

The Closing Disclosure is another critical document that shares similarities with the LSU, especially regarding its role in the closing process of buying a home. It outlines the actual fees, costs, and credits associated with the mortgage, much like the LSU's section on loan terms and conditions. Delivered at least three days before the closing, it ensures the buyer understands all financial aspects of the transaction. The key difference lies in its timing and specificity: the Closing Disclosure provides final details, whereas the LSU offers updates throughout the process.

The Pre-Qualification Letter, often a borrower's first step in the home buying process, presents scenarios akin to those described in the LSU. This document indicates a lender's preliminary assessment of a borrower's creditworthiness and an estimate of how much the borrower might afford. Like the LSU, it informs both buyers and sellers of the prospective buyer's financial standing, yet it precedes the more detailed and process-specific information found in the LSU, serving more as an initial indication rather than an ongoing update.

The Appraisal Report, though primarily focused on assessing the value of the property being purchased, indirectly complements the information found in the LSU. It is critical in determining whether the amount of the loan is appropriate relative to the property's value. Similar to parts of the LSU that might address appraisal requirements and outcomes, the Appraisal Report directly influences the loan's approval process. While the LSU encompasses a broad range of loan status details, the Appraisal Report specifically ensures that the property value aligns with the loan amount, directly affecting the loan's viability.

Dos and Don'ts

When tackling the Arizona Loan Status Update (LSU) form, navigating the process with accuracy and attentiveness is crucial for both buyers and sellers in a real estate transaction. To ensure this document is completed correctly, here’s a concise guide highlighting the dos and don’ts.

Do:

- Ensure that submission of the AAR Loan Status Update (LSU) to the seller occurs within five days after contract acceptance, as stated in Section 2e of the Contract.

- Accurately indicate the lender’s information, including company name, Arizona License number, and the loan officer’s NMLS number, to maintain clear communication.

- Fully complete the Pre-Qualification Information section, noting all relevant loan, buyer, and property details to provide a comprehensive loan overview.

- Check the boxes accurately reflecting the buyer’s situation regarding reliance on the sale or lease of property and seller concessions, as these factors significantly impact the loan qualification process.

- Provide precise information on the type of loan, occupancy type, and property type to avoid any misunderstandings or misrepresentations in the loan process.

- Complete all initial requested documentation information, including Paystubs, W-2s, tax returns, and any pertinent financial records to support the loan application.

- Carefully review and ensure that all parties have signed the document and that all dates are accurate and in compliance with the contract terms.

Don’t:

- Delay in providing the LSU to the seller, as failing to adhere to the five-day requirement can lead to unnecessary complications or delays in the transaction.

- Omit any lender or loan officer contact information, as this can hinder essential communication between the involved parties.

- Leave sections incomplete or provide inaccurate information in the Pre-Qualification Information section, as this could mislead sellers or delay the financing process.

- Incorrectly mark the buyer’s reliance on the sale or lease of property and request for seller concessions, as this can affect the terms and outcome of the loan.

- Misclassify the type of loan, occupancy, or property type, as these details are critical for the appropriate processing and approval of the loan.

- Forget to include all requested documentation, such as financial statements or proof of income, which are essential for a thorough evaluation of the buyer’s loan eligibility.

- Exclude any signatures or date the document inaccurately, as every signature and date is crucial for verifying agreement and compliance with contractual obligations.

By following these guidelines, participants in a real estate transaction can ensure a smoother, more efficient process when completing the Arizona Loan Status Update (LSU) form. This not only fosters transparency and trust between the buyer, seller, and lender but also paves the way for a successful property transaction.

Misconceptions

There are several misconceptions about the Arizona Loan Status Update (LSU) form that can confuse both buyers and sellers in real estate transactions. To clarify, here's a list of common misunderstands and the truth behind them:

- Misconception 1: The LSU form is optional for the buyer to complete.

Fact: It’s a critical document required to be submitted within five days after contract acceptance, ensuring that the seller is aware of the loan's status.

- Misconception 2: The LSU form only needs to be filled out once.

Fact: The buyer must instruct the lender to provide updated LSUs to the seller and broker upon request, ensuring ongoing communication about the loan status.

- Misconception 3: The LSU form is complex and filled with legal jargon.

Fact: While it is a legal document, it’s designed to be straightforward, outlining the loan's current status in accessible terms.

- Misconception 4: Any lender can complete the LSU form.

Fact: The lender indicated on the form, with their Arizona license and NMLS numbers, is responsible for its completion.

- Misconception 5: The buyer’s marital status has no impact on the LSU.

Fact: Marital status can affect loan approval and terms, making it a necessary detail on the LSU form.

- Misconception 6: The LSU form covers only the basics of the buyer’s financial situation.

Fact: It includes detailed pre-qualification information like income, assets, and debts, along with the type and terms of the loan.

- Misconception 7: Sellers are not entitled to updates after the initial LSU submission.

Fact: The seller, upon request, has the right to receive updated LSUs, maintaining transparency throughout the closing process.

- Misconception 8: The LSU does not require the buyer’s acknowledgement to proceed with the lender.

Fact: The form includes a section where the buyer acknowledges their intention to proceed with the specified lender under the described terms.

- Misconception 9: All sections of the LSU must be completed for every transaction.

Fact: Some sections may be marked as not applicable (N/A), depending on the specifics of the loan and property type.

- Misconception 10: The closing section of the LSU is only for the lender’s use.

Fact: While the lender completes this section, it provides crucial information for both the buyer and seller about the closing documentation, underwriting, approval, and escrow process.

Understanding these details about the Arizona LSU form ensures a smoother real estate transaction for all parties involved, promoting clarity and reducing the potential for misunderstanding.

Key takeaways

Filling out and using the Arizona Loan Status Update (LSU) Form is a critical step in the home buying process, ensuring clear communication between the buyer, seller, lender, and brokers involved. Here are seven key takeaways to help navigate through this important document:

- Timeliness is Crucial: The buyer must deliver the AAR (Arizona Association of REALTORS®) LSU to the seller within five days after the acceptance of the contract. This tight timeframe underscores the importance of punctuality in keeping the purchasing process on track.

- Lender’s Duty to Update: The buyer instructs the lender to provide updated LSUs to both brokers and the seller upon request. This requirement ensures that all parties remain informed about the status of the loan application throughout the process.

- Comprehensive Loan Details: The LSU form captures detailed information about the proposed loan, including the type of loan, occupancy type, property type, and whether the buyer is relying on the sale or lease of another property to qualify for this loan.

- Pre-Qualification Disclosure: The form includes sections that detail pre-qualification information, such as discussions of income, assets, and debts, along with a tri-merged residential credit report. It even specifies the pre-qualifying loan amount and the anticipated monthly repayments.

- Verification of Initial Documentation: A checklist of initial requested documentation from the buyer is included in the form. This list encompasses paystubs, W-2s, tax returns, and proof of down payment, among others, ensuring buyers understand what is needed from them upfront.

The LSU mandates proactive communication, with the buyer and lender agreeing to provide loan status updates within five days of contract acceptance and thereafter upon request. This ensures all parties are in the loop concerning any developments or changes. - Final Steps Before Funding: The form outlines the steps required before closing can occur, including underwriting approval, appraisal review, and securing loan approval without conditions. It also details the order and receipt of closing documents and confirmation that all funds have been received by the escrow company.

Understanding and accurately completing the Arizona LSU form is not just a procedural requirement; it's a foundation for a transparent and efficient home buying process. By keeping these key takeaways in mind, buyers, sellers, and their respective agents can navigate this critical stage with more confidence and clarity.

Discover Common PDFs

Arizona Repo Affidavit - A foundational document for lienholders in Arizona, ensuring the repossession and potential sale of a vehicle is conducted within the bounds of state law.

Medical Prior Authorization Form - Applicants are reassured that their Social Security numbers will be used responsibly and exclusively for verification purposes, emphasizing respect for privacy in the process.

Az Business Account Update Form - The DWM156 form serves as Arizona's official Public Weighmaster application, geared towards professionals with scales ready for commercial use.